Trapped by Low Mortgage Rates? The Complete 2026 Guide to Breaking Free

You bought your home in Barrow County in 2021 at 3.25%. Now your growing family needs four bedrooms instead of three, but the mortgage calculator shows your payment would jump $800 per month. So you stay cramped, frustrated, and stuck. Sound familiar?

More than half of all homeowners—51.5%—carry mortgage rates at or below 4%, and nearly seven in ten have rates below 5%. For many Greater Athens area families, that “too good to lose” payment has become a steel trap, even when life clearly says it’s time to move.

As of Q3 2025, mortgages above 6% surpassed those below 3% nationally for the first time—marking a critical inflection point that continues to reshape the market in early 2026. At the same time, roughly one‑third (32.8%) of homes sold in the first half of 2025 were paid for in all cash—well above the pre‑pandemic average of 28.6%. That means about 1 in 3 buyers you compete with are not dealing with rates at all.

The good news: you’re not trapped. This guide breaks down five practical strategies buyers and sellers in Walton, Barrow, Jackson, Gwinnett, Oconee, and Clarke counties are using right now to beat the lock‑in effect without gambling on rate predictions.

PROFESSIONAL DISCLOSURE: This educational content is provided by Timothy Carithers, Licensed Realtor with Real Broker, LLC. Georgia Real Estate License #404881. This blog provides general real estate market information and educational content only. It does not constitute legal advice, financial advice, mortgage lending advice, tax advice, or recommendations for any specific transaction.Real estate transactions involve complex legal and financial considerations. Before making any purchase, sale, or financing decision, consult with:

- A licensed real estate attorney for legal guidance and contract review

- A licensed mortgage lender for loan qualification, rate quotes, and financing options

- A CPA or tax advisor for tax implications

- A financial planner for long-term wealth strategy

Understanding the Lock-In Effect in Greater Athens Area

The lock‑in effect is simple: if you locked a 2.75–3.5% mortgage during 2020–2021, trading that for today’s roughly 6.1–6.3% thirty‑year rates feels like financial self‑sabotage. On a $400,000 mortgage, that rate difference can mean an extra $800+ per month in principal and interest alone depending on your scenario.

Monthly Payment Comparison: How Rate Differences Impact Your Budget

Higher rates significantly increase monthly obligations

Research from 2023 showed that about 82% of homeowners felt “locked in” by their current rates, and sentiment has only intensified. By July 2025, a Bankrate survey found 54% of U.S. adults said there was no mortgage rate at which they’d feel comfortable selling.

Meanwhile, life keeps moving—job changes, growing families, aging parents, and veterans returning from deployment needing more suitable housing. In our local market, those pressures are showing up clearly:

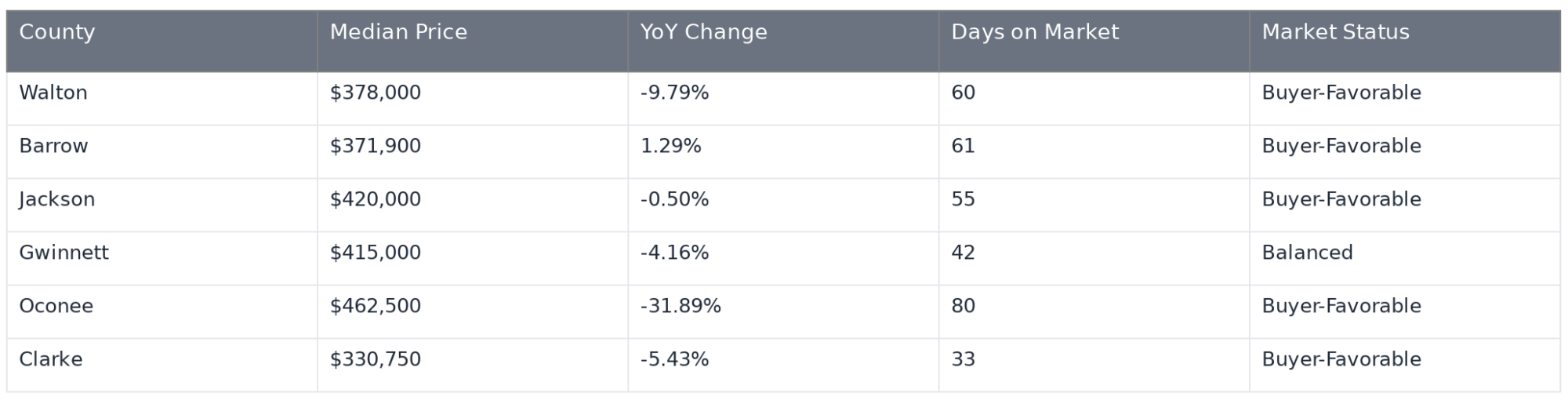

LOCAL AREA MARKET SNAPSHOT (JANUARY 2026)

Most counties showing a buyer-favorable conditions with varying inventory levels

- Barrow County homes now sit on the market about 61days on average—up significantly from January 2025.

- Oconee County’s days on market stays the same while the median home sales have dropped significantly by 31.89% from January 2025.

- Gwinnett County’s active listings have climbed and days on market have stretched to the mid‑40s.

Strategy #1: VA Loan Assumptions—A Game-Changer for Veterans

If you’re a veteran seller in Greater Athens with a VA loan from the 2020–2021 period, your mortgage rate may be the single strongest marketing tool you have. If you’re a veteran buyer, VA assumptions can create affordability that rivals the “good old days.”

Any existing VA loan may be assumable to a qualified buyer—veteran or non‑veteran—subject to the current loan servicer’s approval and VA guidelines. In a successful assumption, the buyer takes over the seller’s remaining balance, interest rate, and amortization schedule, and pays an assumption funding fee that’s typically lower than the standard VA funding fee.

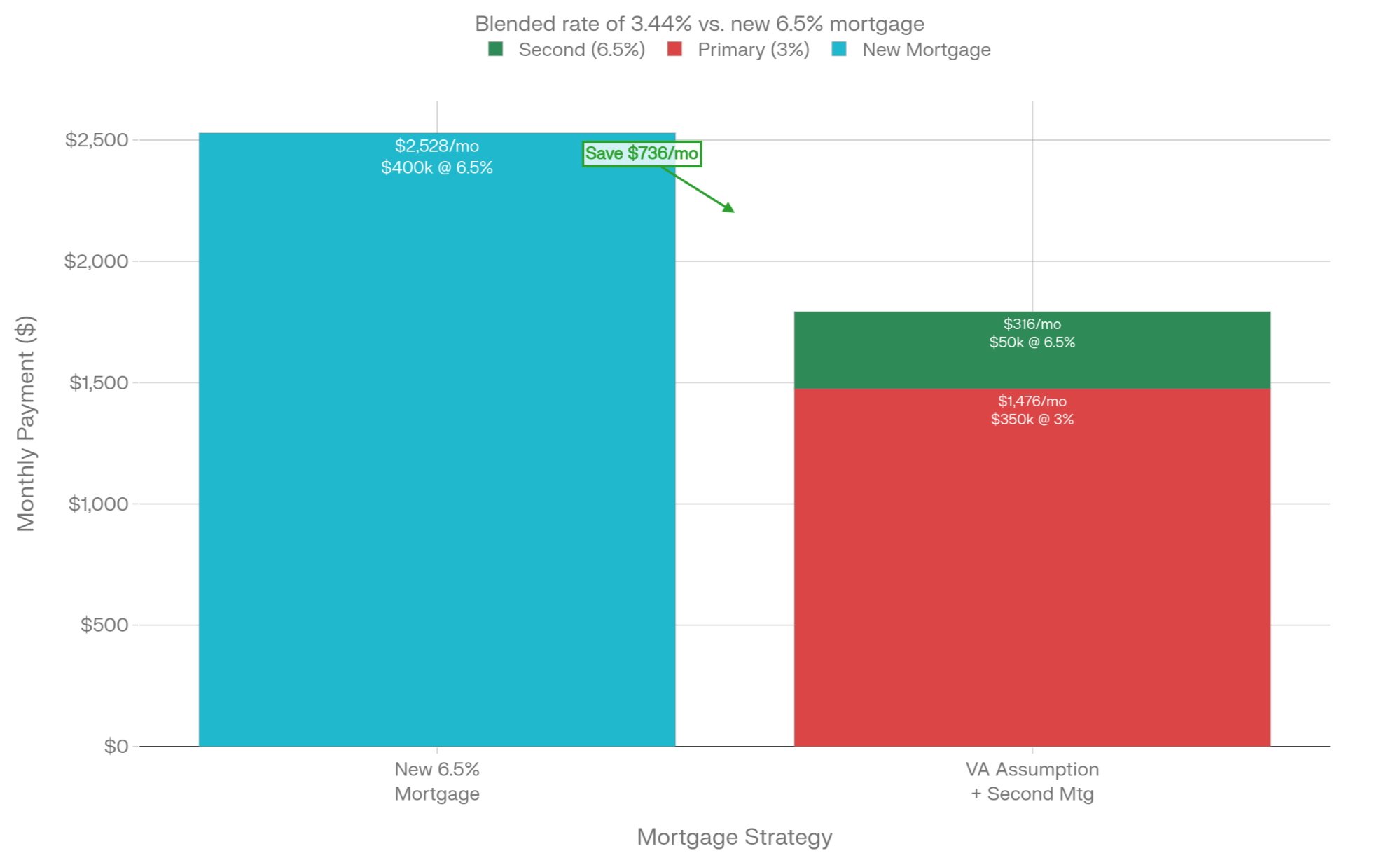

Real Numbers: Why Assumptions Matter

Take a hypothetical Braselton property:

- Price: $425,000

- Existing VA balance: $350,000 at 3.0%

- Equity gap: $75,000

Scenario 1: New 6.5% Mortgage

- Loan: $400,000 at 6.5%

- principal and interest: $2,528/month

- Assumed VA loan: $350,000 at 3.0% ≈ $1,476/month

- Second loan for gap: $50,000 at 6.5% ≈ $316/month

- Total P&I: ≈ $1,792/month

- Effective blended rate: about 3.44% on the combined balance

VA LOAN ASSUMPTION REDUCES MONTHLY PAYMENT BY $736

Note on Secondary Financing: Obtaining a second mortgage or other financing to cover an equity gap requires approval from both the assumption servicer and the lender providing the secondary financing. Not all lenders offer piggyback loans, and qualification requirements vary. Discuss equity gap financing strategies with your licensed mortgage professional during pre-qualification.

Entitlement Considerations (Without Giving Legal Advice)

When VA loans are assumed, entitlement questions matter. VA loan assumptions can involve questions about entitlement restoration and future VA eligibility. These are legal and regulatory matters that depend on buyer status, transaction structure, and VA rules.

As your Realtor, I can raise these issues, but I cannot provide legal interpretations or tell you how your entitlement will be treated. For that, you need a VA‑approved lender and, where appropriate, a real estate attorney. Discuss entitlement considerations, including restoration and substitution, directly with those professionals before you authorize an assumption.

How to Approach VA Assumptions Safely

- Treat assumability as a marketing advantage, not a DIY project.

- Before advertising your loan as assumable, confirm eligibility and guidelines with your loan servicer and a VA‑knowledgeable lender.

- If you’re a buyer, have the servicer outline their current assumption process, timelines, and costs—these can vary widely by lender.

Strategy #2: FHA Assumable Mortgages—Hidden Opportunity for First-Time Buyers

FHA-backed mortgages also offer assumption potential. FHA guidelines generally allow assumptions on qualifying loans originated after December 15, 1989, subject to servicer approval.

For first‑time and budget‑sensitive buyers in Walton, Barrow, Jackson, and Gwinnett counties, that can be a lifeline when FHA loans written at 2.75–3.75% are still out there.

Key Concepts (High-Level, Not Legal Advice)

FHA typically requires a minimum 580 credit score and 43% debt‑to‑income ratio, though individual lenders may have higher requirements and additional overlays. The servicer must approve the assuming buyer, and there is usually a capped assumption fee that is often lower than full loan origination costs.

Assumption Qualification Note: The qualification requirements and timelines for FHA assumptions vary by lender. The 580 credit score and 43% DTI often cited are FHA program minimums, not guarantees. Many servicers require higher scores, lower DTIs, or additional reserves. Before planning around an assumption, obtain pre‑qualification from the specific lender servicing the loan and confirm that the loan is assumable under their current policy.

Handling the Equity Gap

Because the buyer only takes over the seller’s remaining FHA balance, the difference between that balance and the agreed purchase price—the equity gap—must be covered through:

- Cash from the buyer

- A second mortgage or other financing acceptable to the servicer

- Structured arrangements such as a seller-held second lien (when permitted by the lender and compliant with law)

Given the legal complexity, lien priority issues, and the importance of proper documentation, any FHA assumption involving secondary financing should be coordinated with both a lender and a Georgia real estate attorney. As your Realtor, I can help coordinate the team, but I don’t draft documents or structure the legal side.

Strategy #3: 2-1 Temporary Buydowns—Short-Term Relief With Long-Term Planning

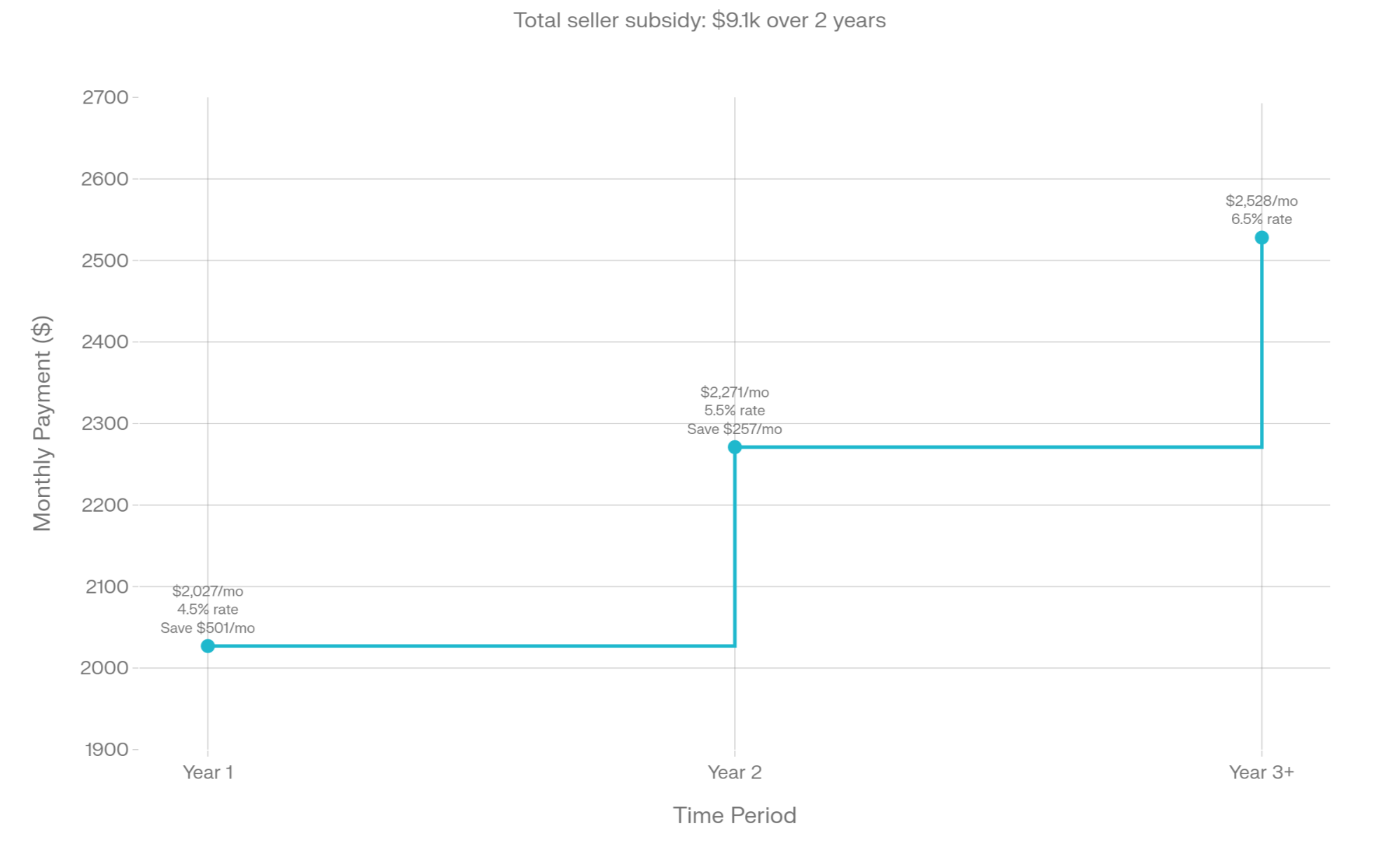

A 2‑1 temporary buydown is a tool where a lump‑sum contribution (often from the seller) lowers the buyer’s interest rate by 2% in year one and 1% in year two before reverting to the full note rate.

On a $400,000 loan at a 6.5% note rate, a typical 2‑1 buydown might look like this:

Depending on lender specifics and the exact structure, the total cost to fund that buydown often falls in the $9,000–$10,000 range for a $400,000 loan at current rate levels, though exact amounts vary by program and rate environment.

- Year 1: payment based on 4.5%

- Year 2: payment based on 5.5%

- Year 3+: payment based on 6.5%

Depending on lender specifics and the exact structure, the total cost to fund that buydown often falls in the $9,000–$10,000 range for a $400,000 loan at current rate levels, though exact amounts vary by program and rate environment.

2-1 BUYDOWN REDUCES PAYMENT IN EARLY YEARS ($400K LOAN)

This structure can:

- Help payment‑sensitive buyers ease into homeownership as income grows.

- Give marginally qualified buyers a better chance at approval by lowering initial payments, subject to lender guidelines.

- Provide a more powerful concession than a comparable price cut in a buyer‑favoring market like today’s Greater Athens environment.

Strategy #4: Seller Financing—Powerful but Highly Regulated

Seller financing (owner financing) is when the seller agrees to receive payment over time instead of the buyer using a traditional lender. It can unlock deals that otherwise wouldn’t work, especially for buyers with unusual income profiles or when appraisals lag market reality.

Typical structures often include:

- A negotiated down payment (commonly 10–20%)

- A written promissory note outlining repayment terms

- A deed of trust or security instrument giving the seller a lien on the property

Critical Compliance Considerations

Seller Financing Regulatory Notice: Seller financing involves federal Truth in Lending Act (TILA) disclosure requirements, including disclosure of the annual percentage rate, finance charges, amount financed, and total payments. Sellers who regularly offer seller financing may be subject to SAFE Act licensing requirements. Georgia law also requires specific disclosures and documentation standards for residential seller financing transactions. Because of the complexity of these federal and state rules, any seller considering owner financing MUST consult with a real estate attorney and, where appropriate, compliance-savvy lenders or advisors to ensure proper documentation, disclosure compliance, and legal protection. Failure to comply with TILA and related disclosure requirements can result in federal penalties and potential contract enforceability issues.

Given these layers:

- I donot set interest rates, draft notes, or design balloon structures.

- My role is to help you evaluate whether seller financing might make sense strategically and connect you with Georgia attorneys and mortgage professionals who can structure it correctly.

Strategy #5: Portable Mortgages—Concept, Not Contract

You may have seen headlines about “portable mortgages” that let you take your low rate with you when you move. It’s an attention‑grabbing idea, but it’s important to be precise about where things stand.

The FHFA has stated it is exploring the concept of portable mortgages, but no timeline, program details, or implementation plan has been announced. This remains a theoretical discussion subject to regulatory approval, market feasibility, and policy development that may or may not occur.

In other countries like Canada and the UK, portable structures often let borrowers transfer an existing balance and rate to a new property and then layer new debt at current rates. If some version is ever adopted here, it could ease the lock‑in effect for certain move‑up buyers, but it could also have complex ripple effects on pricing and equity.

This section discusses a policy concept under early exploration with no announced timeline or certainty of implementation. Homebuyers and sellers should not make purchasing decisions based on the potential availability of portable mortgages.

My job is to track these developments so that if and when a real, regulated product appears, you already understand the basic idea and can have informed conversations with lenders and attorneys.

Mortgage Math: Helpful, But Not a Promise

The payment and blended‑rate illustrations in this guide are there to make the concepts concrete. They’re not quotes, offers, or guarantees.

Mortgage Payment Disclaimer: The payment calculations shown here are illustrative examples using standard amortization concepts and publicly available rate ranges. They do not reflect actual loan offers. Your actual monthly payment will vary based on your credit profile, loan type, down payment, discount points, lender fees, property taxes, homeowner’s insurance, HOA dues, and current market rates at the time of rate lock. These examples do not include closing costs, prepaid expenses, or escrow requirements. For accurate payment calculations and pre‑qualification, contact a licensed mortgage lender.

Putting It Together: A Practical Framework

When you’re deciding how to move forward, it helps to have a simple lens instead of drowning in options.

VA or FHA Assumptions May Fit When:

- The existing loan has a significantly lower rate than current market levels.

- There’s a meaningful remaining balance, not just a small leftover mortgage.

- You can realistically address the equity gap (cash, DPA, secondary financing, or combination).

- The current servicer confirms assumability and outlines their process.

- You qualify for the full payment but want payment relief in the first two years.

- You expect income to grow (promotion, second earner returning to work, commission ramp‑up).

- You’re buying in a market segment where sellers are negotiating concessions.

- The seller owns the property free and clear or has small remaining debt.

- Traditional financing is blocked by non‑credit issues (e.g., non‑standard income documentation).

- Both parties are willing to invest in legal and compliance counsel to structure the deal correctly.

- There isn’t enough remaining balance on the existing loan to make assumptions worth the complexity.

- Cash offers dominate your target price range and you need certainty and speed.

- The rate gap between existing loans and current market offerings has narrowed enough that flexibility, speed, or simpler terms matter more than chasing the lowest possible rate.

Legal and Professional Boundaries (So You’re Protected)

As your Realtor, I can connect you with the right property, help you interpret market conditions, negotiate terms, and coordinate the transaction. I cannot provide legal interpretations, draft legal documents, or advise on legal strategies. For anything touching contracts, title, disclosures, seller financing documents, or VA/FHA legal rights, I will always recommend you work with a qualified real estate attorney and lender licensed to operate in Georgia.

The same applies on the lending side: I’ll help you understand the big‑picture differences between tools like assumptions, buydowns, and conventional financing, but only a licensed loan officer can issue rate quotes, underwrite your file, or tell you what you personally qualify for.

Staying in the right lane is part of how I protect you.

What This Means for You in Greater Athens area

If you’re sitting on a 3–4% mortgage in Walton, Barrow, Jackson, Gwinnett, Oconee, or Clarke County and feeling paralyzed, you’re not stuck—you’re just operating with an incomplete toolkit.

- Veterans can sometimes unlock serious negotiating power by marketing properly structured, assumable VA loans and pairing them with informed entitlement and legal guidance from their lender and attorney.

- First‑time buyers facing 6%+ rates can improve affordability by targeting assumable FHA/VA loans, combining them with Georgia DPA programs, or negotiating 2‑1 buydowns instead of only chasing price cuts.

- Strategic homeowners who “need to move but hate today’s rates” can use these tools to narrow the gap between quality‑of‑life needs and financial reality.

Next Step: Build the Right Team

Thinking about buying or selling in Greater Athens but concerned about current mortgage rates? Let’s sit down and talk through your situation. I’ll help you clarify your goals, then connect you with trusted mortgage professionals and real estate attorneys who can explore which strategies—including assumable mortgages, temporary buydowns, seller financing, or traditional loans—may fit your unique circumstances.

From there, my role is to help you:

- Identify properties—or buyers—where these strategies actually apply.

- Coordinate with your lender and attorney so the real estate side of the transaction stays smooth.

- Keep your decisions grounded in both the numbersand the reality of your life stage.

Recent Posts

Beat the Georgia Heat — and the Big Bills

Why Isn't My Oconee County Home Selling? A 14-Day Reset Plan for the 2026 Market

How Do Barrow County First-Time Buyers Navigate the Down Payment Assistance Maze Without Getting Burned?

Is 2026 a Good Time for Walton County Veterans to Buy or Sell a Home with a VA Loan?

May Home Maintenance: Protect Your Investment Before the Heat Hits

Should I Sell My Home in Oconee County in 2026 or Wait? (A 3-Step Guide for Real Numbers, Not Headlines)

What Is the Real Step by Step Home Buying Process for First Time Buyers in Walton County (Without Guessing or Getting Burned)?

How Can Your VA Loan Offer Beat Cash and Conventional in Gwinnett County in 2026?

April, Guard Your Home in April: Simple Moves That Protect Value All Year

What Does It Take to Get Your Oconee County Home Ready to Sell — And What Can You Skip?