How Do Barrow County First-Time Buyers Navigate the Down Payment Assistance Maze Without Getting Burned?

By Timothy Carithers | Fidelis Home Partners | Real Broker | Watkinsville, GA

Realtor | Wealth Builder | Marketer

ABR | MRP | VA Loan Specialist | 4th-Generation Oconee County Native

You're renting in Winder, Auburn, or Bethlehem. You got a raise. Someone told you to "just find a grant" for your down payment. You searched. You found acronyms — FHA, USDA, Georgia Dream, Peach Advantage. You found income limits and conflicting online advice. You closed 14 browser tabs and went back to Netflix.

That's the DPA maze. It's not a bad program or a broken system. It's the collision of real help, complicated rules, and generic online content that knows nothing about Barrow County's actual 2026 market — where starter homes often sell in the $280,000–$350,000 range and homes are averaging 63–76 days on market right now. (Data: GAMLS Local Market Data, Barrow County, Q1 2026.)

The problem isn't finding programs. It's knowing how to structure your contract so the help shows up at closing.

This article is for educational purposes only and is not legal, tax, or lending advice. Every buyer's situation is different. Always consult a participating lender for rates, payments, and qualifications, and a real estate attorney or tax professional for questions about contracts, legal obligations, and taxes. Program names, eligibility rules, and benefit amounts change over time — confirm current guidelines with a Georgia Dream-approved lender and the program administrator before relying on any information here, and do not treat this article as a promise that you will qualify for any program.

Why Is 2026 a Sweet Spot for First-Time Buyers Using Assistance in Barrow County?

One number changes everything for first-time buyers this year:

"Active listings in Barrow County are 81% higher than March 2024.

That isn't just an inventory story — that's buyer leverage

that didn't exist 24 months ago."

Active listings reached 649 homes in March 2026, up from 359 in March 2024. As of April 25, 2026, Barrow carried 4.3 months of supply. Average days on market ran 73 days in January, 76 in February, and 66 in March 2026 — homes are sitting 22–41% longer than two years ago. (Data: GAMLS Local Market Data, Barrow County, Q1 2026.) Sellers who might have rejected a 55-day DPA close in 2022 are more open to them now, especially with a strong lender and clear communication.

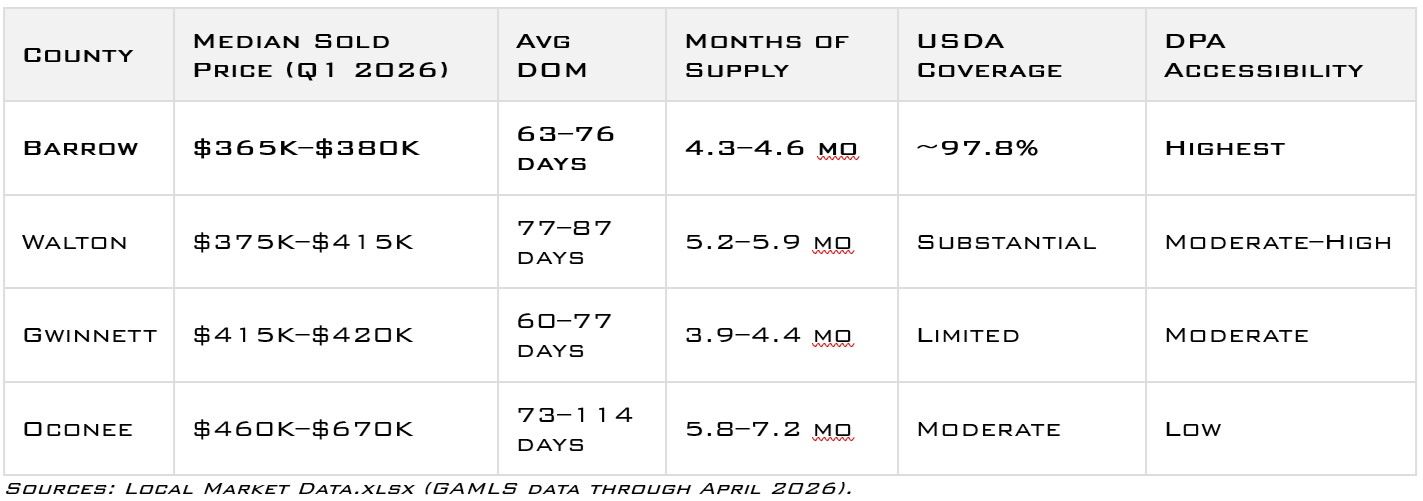

Barrow also has the most favorable price floor and USDA reach of the four counties I work in:

⚠️ All market statistics are based on GAMLS data and public sources through April 2026. Conditions can change quickly. This is for general educational purposes only — not a promise of future market behavior or a guarantee of any specific negotiation outcome.

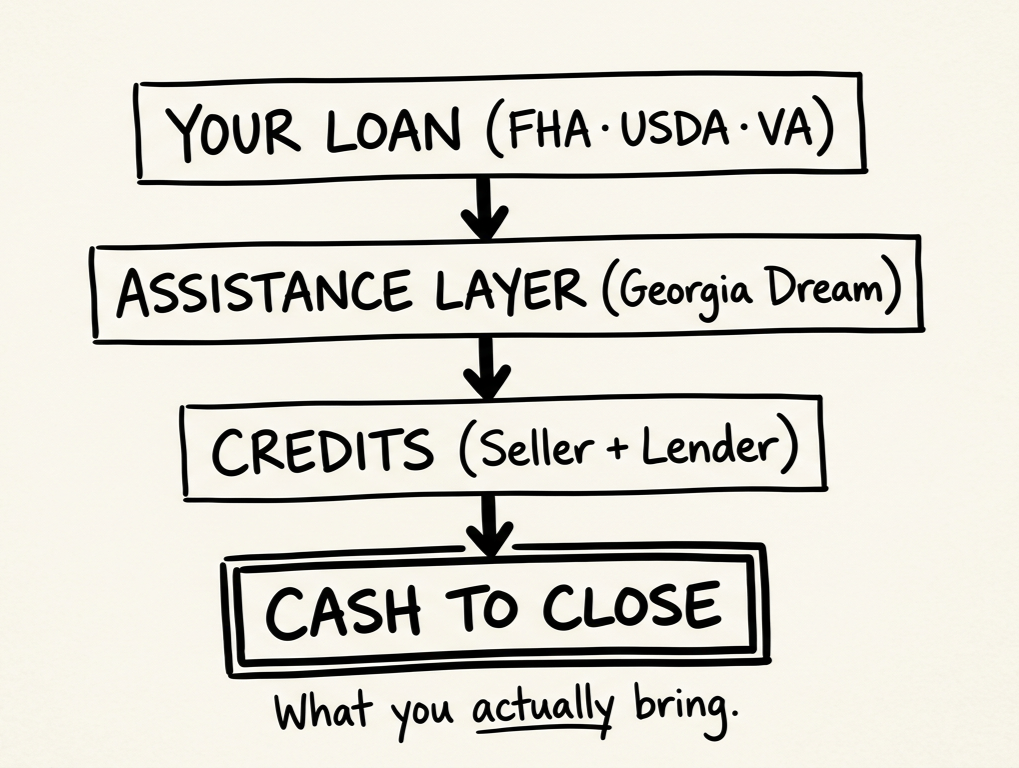

What Does a Smart Barrow First-Time Buyer's "Money Stack" Look Like?

Most DPA information starts with program names. I start with structure. There are three moving parts to your cash-to-close situation: your Loan + Assistance + Credits = your Cash to Close. You don't need to memorize rules. You need to understand the stack and know who handles each piece.

Any numbers in the examples below are for illustration only and are not a quote, commitment, or guarantee. Only a licensed lender can provide actual rate, payment, and cost scenarios for your specific situation.

Building Block 1:

Which Loan Lane Are You Likely In?

Three loan types matter most in Barrow's $275,000–$375,000 DPA band:

- FHA:typically 3.5% down minimum. The 2026 FHA loan limit in this area comfortably clears most Barrow starter homes.

- USDA:zero down in eligible rural areas. Recent mapping shows roughly 8% of Barrow County falling inside current USDA eligibility, including large portions of Winder, Auburn, Bethlehem, Carl, Russell, and Statham. (Each address must be confirmed at the official USDA eligibility map.)

- VA:zero down, no monthly mortgage insurance for eligible veterans with full entitlement. If you have VA eligibility, your money stack looks different — talk to a VA-experienced lender and agent.

My role is helping you focus on neighborhoods and price points where your loan type will appraise well and be accepted by sellers. Qualification is the lender's call.

Building Block 2:

Where Can Assistance Layer on Top?

Georgia's flagship program — Georgia Dream — is built for exactly this buyer. For Atlanta-MSA counties like Barrow, current limits include meaningfully higher income caps and a maximum purchase price that comfortably clears most Barrow starter homes. The assistance takes the form of a 0% interest second loan with no monthly payment, deferred until you sell, refinance, or pay off the first mortgage. Those aren't the outdated limits still circulating online — Georgia Dream is relevant to a much broader range of Barrow working households than most renters realize. Unlike Gwinnett, Barrow doesn't have a county-level DPA program, which means the right lender relationship is everything. A lender who doesn't regularly work with DCA programs won't know how to hit the right timelines or explain the second-lien structure to a listing agent.

⚠️ Program names, eligibility rules, and benefits change over time. Before relying on Georgia Dream, Peach Advantage, or any other assistance program, confirm current guidelines with a participating lender and the program administrator.

Building Block 3:

How Do Seller Credits Change Your Cash to Close?

The average Barrow County transaction closed at 96.6% of original list price in March 2026. (Data: GAMLS.) That gap — combined with homes sitting 66–76 days on market — creates real room to layer seller-paid closing costs on top of DPA. FHA and USDA generally allow sellers to contribute up to 6% of the purchase price toward buyer closing costs. (Confirm allowable uses with your lender — maximums vary by loan type.)

On a sample $315,000 purchase with Georgia Dream DPA and 2% in seller-paid concessions, a buyer's cash-to-close can, in some cases, drop to near the minimum required personal contribution. (Illustration only — not a quote or guarantee. Your lender provides actual figures.)

How Does a Barrow First-Time Buyer Move Through This Maze Step by Step?

Step 1:

Get Clear on Your Comfort Zone Before You Call a Lender

Before a lender touches your credit file, get your own numbers straight:

- Define acomfort payment range, not just a maximum approval.

- List your current debts and a rough sense of your credit tier.

- Narrow your target area: Barrow primary, Walton next, Gwinnett/Oconee if proximity to work shifts the equation.

- Pull together two pay stubs, two years of W-2s or tax returns, and a sense of your savings. Show up to that lender call ready to move.

Step 2:

Pick Barrow Targets Where Your Loan and Assistance Fit

Not all Barrow communities are equal for a DPA buyer:

- Winder (30680):many residential neighborhoods and new-construction communities on the outer rings — including options starting in the low-to-mid $300s — fall within USDA-eligible areas. The denser blocks closest to downtown are more likely to be exceptions.

- Auburn (30011):largely USDA-eligible, with the most densely built commercial corridors potentially excluded.

- Bethlehem, Carl, Russell, Statham:broad USDA coverage with relatively few exclusionary pockets.

Homes in the $280,000–$350,000 band fit comfortably within Georgia Dream and FHA limits and represent a meaningful share of active Barrow inventory. I'm not saying a specific house qualifies — I'm helping you focus your search where the stack tends to work more often.

⚠️ USDA property and income eligibility must be confirmed using the official USDA eligibility map (eligibility.sc.egov.usda.gov) and a participating lender. City-level guidance indicates likely eligibility, not guaranteed eligibility. Your lender will confirm current USDA income limits for your household size.

Step 3:

Structure the Offer Like a DPA Buyer Who Knows the Game

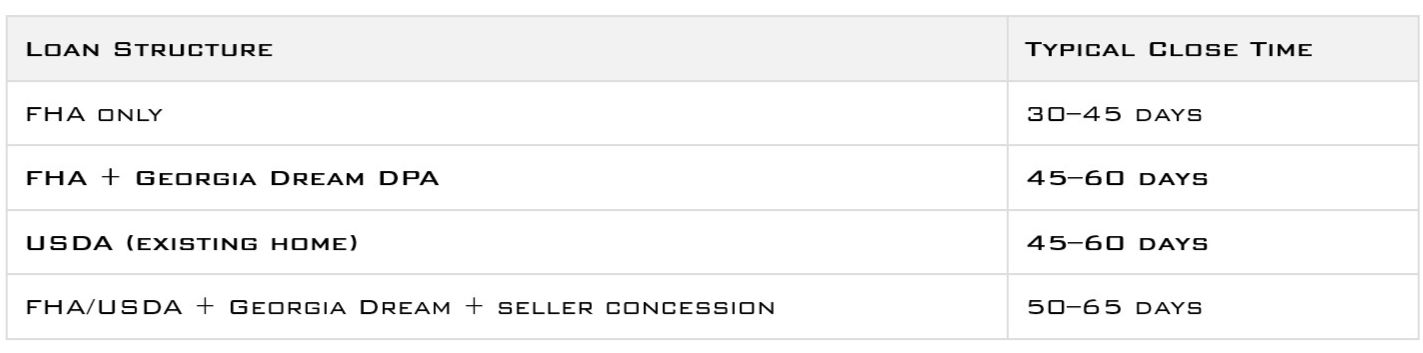

DPA loans take longer. Here's what's realistic in Barrow right now: (Ranges are based on recent experience — not guarantees. Actual times depend on lender capacity, appraisal turns, title, and documentation speed.)

Sellers with homes past 45 days on market are often more open to 50–60 day close timelines when a buyer arrives with a strong pre-approval from a DCA-participating lender and documentation showing DCA funds are already reserved. That documentation piece matters more than most buyers know.

What Does It Feel Like to Use DPA in Barrow with an Agent Watching Your Six?

Scenario: A Barrow Couple Who Thought They Needed 20% Down

A couple renting in Winder — combined income around $85,000, first in their families to buy, targeting the $310,000–$320,000 range. (Illustrative scenario — not a quote or guarantee. Only a licensed lender can provide actual figures.)

Their starting point: "We don't have $25,000 saved. We'll never get there."

Here's what happened when the stack lined up:

- Income qualified under the Atlanta MSA Georgia Dream limits in place at the time.

- Georgia Dream DPA covered a meaningful share of required down payment at 0% interest, deferred until they sell or refinance.

- A seller on a home listed 50+ days accepted 2% in closing cost concessions rather than take another price reduction.

- Their required personal contribution: $2,000.

The shift they needed wasn't more money. It was the right plan and someone to execute it without letting a paperwork gap or a misread timeline blow the deal.

I'm a Marine Realtor helping veterans, homeowners, and first-time buyers build generational wealth through smart and simple home buying and selling strategies in Oconee, Walton, Barrow, and Gwinnett Counties, based in Watkinsville, GA.

⚠️ Program names, eligibility rules, and benefits change over time. Before relying on Georgia Dream or any assistance structure, confirm current guidelines with a participating lender and the program administrator.

How Does a Realtor Protect You When Your Whole Plan Depends on Assistance?

Most buyers spend their energy qualifying for a program. The real challenge is what happens between contract and closing.

Timeline and Paperwork Risk: A missed document request or a close date that ignores DCA's approval window doesn't just delay closing — it can void the assistance entirely. I write realistic close dates matched to the loan type's actual processing window, negotiate with listing agents nervous about longer timelines, and stay ahead of GAR contingency deadlines from contract to close.

Property and Appraisal Risk: FHA and USDA loans carry Minimum Property Requirements. An older Barrow resale with deferred maintenance can trigger repair requirements that stall or kill a DPA deal. I pre-screen for obvious appraisal pitfalls before you go under contract and help you navigate inspection findings with your DPA timeline in mind — not just the inspection report in isolation.

Program Fit vs. Your 5–10 Year Plan: Georgia Dream DPA is a deferred second lien, not a grant. It's repaid when you sell, refinance, or pay off the first mortgage. That's a smart structure for a buyer building equity long-term. For someone who might move in 2–3 years, the repayment math looks different. I don't give legal or tax advice — I ask the question before you're under contract, then point you to your lender and closing attorney for the actual numbers.

What's Your Next Step If You're a Barrow First-Time Buyer?

The shift I want you to walk away with: from "I'm stuck because I don't have 20% down" to "I know the steps and who needs to be on my team."

You don't need to master every program rule. You need a DPA-experienced lender, a Realtor who knows how to build a DPA contract in Barrow's 2026 market, and a closing attorney.

- Request the free Barrow County First-Time Buyer Cash-to-Close Checklist— it walks through every cost category your lender will ask about.

- Book a 20–30 minute "First-Time Buyer Cash Game Plan" call— I'll map your comfort payment range, narrow down Barrow's best DPA-friendly communities, and connect you with 1–2 DPA-savvy local lenders.

Reach out directly:

Timothy Carithers | Fidelis Home Partners | Real Broker | Watkinsville, GA

Serving Oconee, Walton, Barrow & Clarke Counties

📞 706.818.0813 | 📧 t.carithers@fidelishomepartners.com

Google Business Profile

SEMPER FI

Nothing in this article creates an agency relationship or guarantees that any buyer or seller will achieve a particular result. Real estate markets change quickly, and all information here is subject to change without notice. Data is based on sources believed to be reliable as of early 2026, including GAMLS Local Market Data through April 2026, Georgia Department of Community Affairs program guidelines, and USDA property eligibility data — verify current statistics, loan guidelines, and program rules with your own professionals before making decisions. This article is not a loan estimate, offer of credit, or commitment to lend.

Recent Posts