Is 2026 a Good Time for Walton County Veterans to Buy or Sell a Home with a VA Loan?

DISCLAIMER: This blog provides general educational information about Walton County's housing market and VA loan benefits as of April 2026. It is not legal, financial, tax, or lending advice. Market data, rates, and programs change frequently. Veterans should consult a VA-approved lender, licensed real estate agent, tax advisor, and/or real estate attorney for guidance specific to their situation. Timothy Carithers is a licensed Georgia real estate agent and does not provide mortgage, legal, or tax advice.

The short answer:

For the right veteran, 2026 may be one of the better buying windows Walton County has seen since 2019.

Three things are stacking in veterans' favor right now. First, Walton County's market has genuinely rebalanced — homes are sitting longer, sellers are negotiating, and the multiple-offer chaos of 2021–2023 is gone. Second, the structural advantages of a VA loan — zero down, no PMI, and seller concession capability — carry more real-world weight in a slower market than they ever did when cash buyers dominated. Third, Georgia-specific veteran benefits, including existing disabled veteran property tax exemptions and proposed new relief under SB 129, can meaningfully change the true cost of ownership in ways that national VA calculators completely miss.

But the answer isn't the same for every veteran. Selling a low-rate VA home is a different conversation than buying your first. Waiting with a plan can be just as smart as moving now. What follows is the clearest picture I can give you of what's actually happening in Walton County's 2026 housing market — and what that means for your specific situation.

DISCLAIMER: This article is for educational purposes only and is not legal, tax, or lending advice. Every veteran's situation is different. Always consult a VA-approved lender for rates, payments, and qualification, and a real estate attorney or tax professional for questions about contracts, legal obligations, and taxes.

What Is Actually Happening in Walton County's Housing Market in 2026?

How Is the Walton County Market Behaving Right Now?

The defining story of Walton County's 2026 housing market is inventory expansion and normalization — not a crash, not a boom. This is a market that has reset from pandemic-era extremes and is now operating in what the National Association of Realtors® describes as a "balanced" range.

Here's what the data shows, according to Georgia MLS records for Walton County:

- Median sold price, Q1 2026: $375,000–$415,000 (January: $376,500 | February: $415,000 | March: $375,000)

- Median list price, Q1 2026: $453,950–$475,000 — sellers listing meaningfully above where the market is currently clearing

- Active listings, March 2026: 709 — up 14.72% year-over-year from 618 in March 2025

- Average days on market, Q1 2026: 79–87 days — compared to 60–66 days in Q1 2024

- Months of supply (12-month trailing): 5 months — squarely in the balanced market range (the general industry guideline is 4–6 months)

- Sale-to-list price ratios, Q1 2026: 5%–96.7% — indicating many homes are closing below original asking price

(Data: GAMLS Local Market Data, Walton County, Q1 2026. Individual property results vary by condition, location, and seller circumstances.)

This is not a distressed market. Walton County prices are still well above pre-pandemic levels. What changed is the dynamic between buyers and sellers — and that shift creates real, executable opportunity for veterans using VA loans.

What Does This Rebalancing Really Mean for Veterans Using VA Loans?

In the 2021–2023 seller's market, VA advantages got swamped by speed and cash — sellers had ten offers by the weekend, and VA buyers routinely lost.

That market is gone in Walton County right now.

With average days on market running 79–87 days and sale-to-list ratios showing homes regularly closing below asking price, sellers in 2026 need to close deals. Which means VA loan advantages are executable again, not just theoretical:

- Zero down payment for eligible veterans with full entitlement

- No private mortgage insurance (PMI) — which can save roughly $150–$250 per month compared to a conventional loan with less than 20% down

- Seller concessions up to 4% of the loan amount — on a $400,000 purchase, that's potentially up to $16,000 that can cover closing costs, prepaid items, or the VA funding fee

- VA appraisals currently running approximately 7–14 business days — far less disruptive in an 81-day-average-DOM market than in a 72-hour bidding war environment

For veterans who have been sitting on the sideline waiting for "the right time," the real question isn't whether 2026 is perfect — it's whether current conditions align with your actual life situation.

Is There Enough Inventory for Buyers?

Yes — and this matters specifically for VA buyers, who need time to conduct due diligence and move through the appraisal process without pressure. With 599–709 active listings in Walton County as of spring 2026 and new listings up 28% year-over-year through March, buyers have genuine selection across price points. New construction is adding further inventory in Monroe, Loganville, and Social Circle, with several builder communities accommodating VA financing in their programs.

DISCLAIMER: Builder incentive programs change frequently. Verify current availability directly with builders, compare total loan costs across multiple lenders, and consult a VA-approved lender for qualification specifics before committing to any program. VA loan qualification for rate buydown programs is based on the note rate — not the temporarily reduced rate — which affects the loan amount you qualify for.

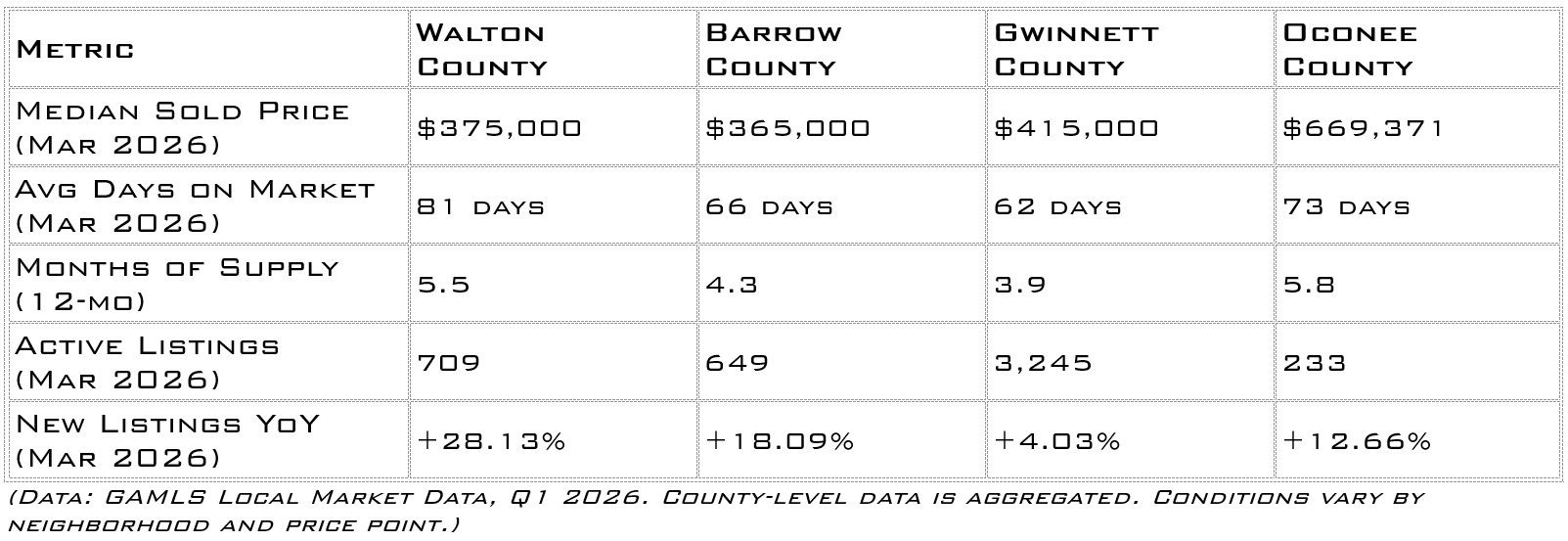

How Does Walton County Compare to Barrow, Gwinnett, and Oconee for VA Buyers?

Most veterans in this corridor are comparing a few counties at once. Here's what the Q1 2026 data actually shows:

No county is universally "better" for every VA buyer. Your ideal location depends on your employment, commute, budget, school priorities, and lifestyle needs. What this table shows is that Walton County currently offers more inventory selection and longer negotiating windows than Barrow or Gwinnett. Oconee operates in a substantially higher price tier — near double Walton's median — which places it outside the practical range for most VA transactions focused on the $250K–$500K band.

Why Is the VA Loan Structurally Competitive in a Higher-Rate Environment?

One of the most common things I hear from veterans right now: "I'm going to wait until rates drop." But the comparison that matters is total monthly cost — not just the interest rate in isolation.

VA loan rates are often competitive with — and in many cases lower than — comparable conventional options for eligible borrowers. Your actual rate depends on your credit profile, lender, and timing. Only a VA-approved lender can give you a real quote.

DISCLAIMER: Any examples in this article are illustrations, not offers to lend or guarantees that a particular strategy will be right for you. Only your lender can determine whether you qualify for a VA loan, what your rate and payment options look like, and how any specific structure might work in your case.

Here's an illustrative example — not a quote, not a guarantee, and not a substitute for your own lender conversation:

- A veteran purchasing at $375,000 with zero down at an illustrative 6.25% VA rate: estimated principal and interest of approximately $2,309/month — no PMI.

- A conventional buyer at the same price with 5% down at an illustrative 6.75%: estimated P&I of approximately $2,326/month — plus PMI of roughly $160–$200/month until they reach 20% equity.

The gap compounds over time — and that's before Georgia's disabled veteran tax exemptions change the math entirely.

What Should Veteran Homeowners in Walton County Know About Selling with a VA Loan in 2026?

The "rate lock-in" fear is real — but it's not a life sentence. Whether it makes sense to move depends entirely on your specific numbers and life circumstances, not on a national headline.

Is Now a Good Time to Sell My Walton County Home If I Bought with a VA Loan?

Veteran sellers in Walton County's 2026 market need one thing above all else: pricing discipline. With median sold prices running 9–10% below median list prices and homes averaging 79–87 days on market, overpriced listings are sitting while accurately priced listings are selling.

If you purchased your home between 2018 and 2022, you likely hold meaningful equity — even accounting for the modest Q1 2026 softening. Walton County's full-year 2025 trend was still positive, with December 2025 median sold prices at $425,710 according to Redfin data. That context matters when evaluating your net proceeds.

The question for sellers isn't whether the market is "good." The question is whether your equity position, your next housing move, and your life situation make a 2026 sale the right decision for your family. That math is worth running before you decide either way.

Can I Use My VA Loan Benefits Again After I Sell?

Yes — in most circumstances. This is one of the most persistent myths I encounter from veterans: "I already used my VA loan once, so I can't use it again." That's not accurate.

When you sell your current home and pay off the VA loan in full, your entitlement is typically restored, allowing you to use a VA loan again on your next purchase. There are also scenarios where remaining entitlement — sometimes called "bonus entitlement" or "second-tier entitlement" — allows a veteran to purchase again without selling the current home first. The specifics depend on your loan history, remaining entitlement balance, and the loan amount you need.

DISCLAIMER: This is an area where getting the details wrong costs real money. Before making any move, consult a VA-approved lender who can pull your Certificate of Eligibility and walk you through your exact entitlement position. Visit VA.gov for official guidance on entitlement restoration.

What Is a VA Loan Assumption — and Why Can It Be a Selling Advantage?

Here's a feature of VA loans that almost no one in Walton County is actively marketing — but should be: VA loans are assumable.

That means a qualified buyer can take over your existing VA loan at your original interest rate, rather than obtaining new financing at today's rates. If you purchased in 2020 or 2021 at a rate in the 2.75%–3.25% range, a buyer who assumes that loan gets your original rate — not the significantly higher rates currently available in today's market.

In a market where homes are averaging 81 days on the market and sellers are regularly negotiating below asking price, a legitimately assumable VA loan at a below-market rate can attract buyers willing to close closer to your asking price — potentially narrowing the gap between where you want to list and where the market is currently clearing.

DISCLAIMER: Critical - VA loan assumption requires lender approval and full borrower qualification by the assuming buyer. More importantly, you must ensure you receive a full release of liability at closing — otherwise your VA entitlement remains tied to that loan even after the sale. This has real financial and legal implications. Consult your current mortgage servicer, a VA-specialist lender, and a real estate attorney before marketing any home as having an assumable loan.

What Georgia-Specific Veteran Benefits Should Walton County Buyers Know About?

This is the section most national VA content skips entirely — and it's the part that can meaningfully change the real-world math of homeownership for Georgia veterans. I'm going to give you an honest picture with clear guardrails about what is current law versus what is still proposed.

What Property Tax Exemptions Exist Right Now?

Georgia currently offers qualifying disabled veterans a homestead exemption from ad valorem property taxes — state, county, municipal, and school — for veterans who are Georgia citizens, residents, and occupy the home as their primary residence. The exemption amount is the greater of $32,500 or the maximum allowed under 38 U.S.C. § 2102, which was indexed to $121,812 for 2025.

In Georgia, property is assessed at 40% of fair market value. This exemption is applied to your assessed value — not the full market value. The exemption also extends to an unmarried surviving spouse or minor children as long as they continue to occupy the home as their primary residence.

Georgia also provides an additional homestead exemption of $60,000 plus further ad valorem relief for the unremarried surviving spouse of a service member killed in action or who died as a result of war or armed conflict.

DISCLAIMER: To understand exactly how current exemptions affect your specific property tax bill, contact the Walton County Tax Assessor's Office directly and work with your CPA or tax advisor for personalized guidance. This information is educational and does not constitute tax advice.

Could 100% Disabled Veterans Pay Zero Property Taxes Starting in 2027?

If you are a veteran with a 100% Permanent and Total (P&T) disability rating from the VA, this proposed benefit may be the most financially significant development in Georgia veteran homeownership in decades.

Georgia Senate Bill 129 passed the state legislature in the 2025–2026 session and is headed to Georgia voters on the November 2026 ballot. If approved by voters, it would:

- Provide a complete exemption from property taxes on the primary residence for veterans with a 100% P&T VA disability rating

- Provide proportional relief for partially disabled veterans — calculated as their disability percentage multiplied by the assessed home value

- Take effect January 1, 2027 — only if voters approve it

DISCLAIMER: This is proposed legislation, not current law. Do not make any purchasing decision based on the assumption that SB 129 will pass. Use conditional language with your family: "If this passes in November, it could mean..." — not "I will pay zero taxes." Monitor the November 2026 ballot and work with a tax advisor to model your specific scenario under both current law and the proposed change. Contact the Walton County Tax Assessor's Office for current tax information specific to any property you are evaluating.

Does Georgia Offer Any Below-Market VA Loan Programs?

Yes. The Georgia Department of Community Affairs offers the Peach Select VA Loan Program, which pairs VA loan benefits with down payment assistance for eligible Georgia veterans. Program features generally include grant-based down payment assistance and competitive fixed-rate financing. Income limits, purchase price caps, credit requirements, and program terms vary by county and change based on funding availability.

DISCLAIMER: Visit GeorgiaDream.com or contact a Georgia Dream-approved VA lender for current program details before making any financial decisions. All program terms should be verified directly — availability changes based on funding cycles.

How Do I Decide Whether to Buy, Sell, or Wait as a Walton County Veteran in 2026?

This is the real question — not "what does the market look like," but "what should I do?" Here's the framework I walk every veteran through.

What Are the Biggest Advantages for VA Buyers in Walton County Right Now?

For veterans who are financially positioned and have a genuine life reason to move in 2026, the current Walton County market may offer a real window:

- Negotiating room that hasn't existed for years. Sale-to-list ratios of 93.5%–96.7% show the market regularly settling below ask. VA buyers who enter negotiations with current comparable sales data have real leverage.

- Seller concession potential. Up to 4% of the loan amount in seller concessions is VA-permitted. In a market where sellers are motivated and homes are sitting, requesting concessions toward closing costs is a realistic and frequently successful negotiating strategy.

- No PMI — permanently. This isn't a temporary savings. It's a structural advantage of the VA loan over conventional financing at any down payment below 20%.

- Georgia disabled veteran tax benefits. If you carry a service-connected disability rating, the existing Georgia homestead exemption and the proposed SB 129 relief (subject to voter approval in November 2026) could reduce your true monthly ownership cost in ways no national calculator reflects.

- VA funding fee exemption for disabled veterans. Veterans with a service-connected disability rating of 10% or higher are fully exempt from the VA funding fee. On a $400,000 purchase, the standard 2.15% first-use fee equals approximately $8,600. That exemption is real money — and it compounds alongside no down payment and no PMI.

What Are the Real Risks and Honest Downsides?

- Rates are elevated. Current VA rates are meaningfully higher than the historic lows of 2020–2021. For some veterans, the monthly payment on a realistic Walton County home may not fit their budget at today's rates — and knowing that now prevents a painful situation later. For some veterans, the monthly payment on a realistic Walton County home simply may not fit their budget at today's rates. That's a real constraint — and knowing it now prevents a painful situation later.

- Prices have not reset to pre-pandemic levels. Walton County's current median of $375,000–$415,000 is still well above 2018–2019 levels. You're buying in an adjusted market, not a discounted one.

- VA appraisals can complicate older resale homes. VA Minimum Property Requirements can occasionally trigger required repairs or reinspection conditions on homes with deferred maintenance. New construction in Walton County is generally cleaner from a VA appraisal standpoint.

- Waiting without a plan is not a strategy. Many economists expect the Federal Reserve may cut rates later in 2026, which historically increases buyer demand and compresses available inventory. Future market conditions are inherently uncertain. If you wait without concrete benchmarks — a savings target, a debt paydown goal, a defined trigger point — you risk being in the same spot twelve months from now, competing against more buyers for the same homes at potentially higher prices.

What's the 3-Step Decision Framework?

Whether you're buying, selling, or genuinely unsure — here's how to move forward without analysis paralysis:

Step 1 — Clarify your 2026 situation and goals.

Where are you now — renting or owning? What's changing in your life over the next 2–3 years? PCS orders, military retirement, family size shift, job change? Do you need more space, less space, or just more stability? This conversation costs nothing and prevents expensive decisions made on incomplete information.

Step 2 — Run your real Walton County numbers — not the internet's.

National calculators don't know Walton County's current price bands, property tax rates, Georgia exemptions, or what a motivated local seller is actually willing to do. Until you see what your actual payment looks like at a realistic local price point — with your income, debts, VA status, and any disability exemptions factored in — you're making decisions with a blurry picture.

Step 3 — Choose a path: buy, sell, or prepare — with a 12–24 month game plan.

If buying now makes sense: get clear on your price range, understand VA offer strategy for Walton's current market, and move with confidence. If selling now makes sense: price accurately from day one, understand your equity position, and have a defined plan for your next housing move. If waiting is right: set specific targets — savings benchmarks, debt paydown goals, a timeline for revisiting the numbers — so you're moving forward with intention, not drifting.

What Are the Key Questions Walton County Veterans Are Asking in 2026?

What is the VA loan limit in Walton County, Georgia in 2026?

For veterans with full VA entitlement — first-time VA loan use or fully restored entitlement — there is no VA loan limit. Loan approval is based on income, debts, and residual income, not a geographic cap. The 2026 baseline conforming loan limit of $832,750 applies statewide in Georgia (Georgia has no high-cost county designations) and primarily matters for partial entitlement calculations. At Walton County's Q1 2026 median prices of $375,000–$415,000, most VA transactions fall well within standard entitlement ranges.

Do I really need a down payment for a VA loan in Walton County?

No down payment is required for eligible veterans with full entitlement. Individual eligibility depends on your specific entitlement status, lender qualification requirements, and property details. Contact a VA-approved lender to confirm your exact position before making any offers.

Can I use my VA loan more than once?

Yes. When you sell your current VA-financed home and pay off the loan, your entitlement is typically restored and available for reuse. In some situations, veterans may be able to use remaining entitlement for a second purchase without selling the first home. Your Certificate of Eligibility — available through VA.gov or a VA-approved lender — shows your exact entitlement status.

What is the VA funding fee in 2026, and who is exempt?

The 2026 VA funding fee for a first-use purchase loan with zero down is 2.15% of the loan amount — approximately $8,600 on a $400,000 purchase. Veterans with a service-connected disability rating of 10% or higher are fully exempt from the VA funding fee. Purple Heart recipients are also exempt. Surviving spouses of veterans who died in service or from a service-connected disability may also qualify for exemption. Confirm your exemption status with a VA-approved lender before closing.

Are VA loans competitive in today's Walton County market?

Yes — more so now than at any point between 2021 and 2023. With homes averaging 79–87 days on market and sale-to-list ratios showing most homes closing below asking price, sellers in Walton County's 2026 market need to close deals. That reality changes the competitive equation.

How long does a VA loan typically take to close in Georgia?

VA purchase loans in Georgia typically close in 30–45 days when using an experienced VA-approved lender and a properly prepared buyer. VA appraisals are currently running approximately 7–14 business days in 2026. In Walton County's current 81-day average DOM environment, that timeline creates no meaningful competitive disadvantage.

What Is the Smart Next Step for Walton County Veterans in 2026?

If you've read this far, you already have more local, specific information about Walton County's VA housing market than most veterans get from ten hours of Googling. But information without a plan is just noise.

Here's what I do with every veteran who reaches out — three steps, clear and direct:

Step 1 — Schedule a 2026 VA Strategy Call (20–30 minutes, Walton-focused)

You bring the questions you've been trying to piece together from national sites, social media, and generic calculators. I bring four-plus years of VA transactions in Walton, Barrow, Gwinnett, and Oconee Counties — plus a Marine's directness about what the numbers actually say for your situation. We cover your branch of service, current housing status, county preference, and any major life events on the horizon. By the end, you'll know whether 2026 is your window or not.

Step 2 — Get Your Personalized Buy / Sell / Wait Numbers

This is where generic advice stops and your actual situation begins. Working alongside a VA-approved lender partner, we build your picture:

- For buyers:Payment ranges at realistic Walton County price points, buy-now vs. wait comparisons that account for likely price and rent movement, and a clear-eyed look at how Georgia's veteran tax benefits affect your true monthly cost.

- For sellers:Current estimated equity position, what a 2026 sale could realistically unlock, and whether using VA entitlement again or exploring other financing options makes the most sense for your next move.

Step 3 — Move Forward (or Wait) With a Clear Plan

If the numbers and your life situation say move now: I'll help you get VA-strong offers ready for Walton County's current market, identify the right price bands and areas that fit your priorities, and make sure your offer communicates strength — not uncertainty — to sellers.

If the numbers say wait with intention: I'll help you set specific 12–24 month benchmarks — debt targets, savings goals, a defined trigger point — so you're never alone in the process and never making a reactive decision based on a headline.

A Final Word to Walton County Veterans in 2026

I've been in Walton and Oconee County my entire life. I've watched this market through multiple cycles. And I've sat across the table from veterans who spent years convinced their VA benefits were too complicated or too risky to actually use — only to realize, once the numbers were clear, that they had been holding one of the most powerful financial tools available to any homebuyer in America.

Your VA benefit wasn't designed for a perfect market. It was designed for real life — PCS orders, transitions, family changes, the moments when you need stability and your service record earns you the tools to create it. In 2026, Walton County's market is more accommodating to those tools than it has been in years.

The goal is not to convince you to buy or sell. The goal is to make sure that if you do move — you do it with clear eyes, real numbers, and a guide who has walked the same road you have.

Ready to run your 2026 VA numbers?

Schedule a no-pressure VA Strategy Call →

Or reach out directly:

Timothy Carithers | Fidelis Home Partners | Real Broker | Watkinsville, GA

Marine Veteran · MRP · ABR · Master Certified in VA Loans

Serving Oconee, Walton, Barrow & Clarke Counties

📞 706.818.0813 | 📧 t.carithers@fidelishomepartners.com

Google Business Profile

SEMPER FI

Recent Posts