What Is the Real Step by Step Home Buying Process for First Time Buyers in Walton County (Without Guessing or Getting Burned)?

If you’re a first-time buyer in Walton County trying to figure this out without a built-in support system, the hardest part is usually not the house itself. It’s the noise: random internet checklists, confusing lender jargon, social media hot takes, and a 2026 market that can feel like it’s changing every time you open your phone.

A smart first-time buyer does not need more hype. A smart first-time buyer needs a clear roadmap, realistic timelines, and a plain-English explanation of what happens before pre-approval, after the offer, and all the way through closing in Georgia.

I’m a Marine Realtor helping veterans, homeowners, and first-time buyers build generational wealth through smart and simple home buying and selling strategies in Oconee, Walton, Barrow, and Gwinnett Counties, based in Watkinsville, GA.

This article is for educational purposes only and is not legal, tax, or lending advice. Every buyer’s situation is different, so talk with a VA-approved lender for rates, payments, and approval, and talk with a real estate attorney or tax professional for questions about contracts, legal obligations, or taxes.

What Does the Full First-Time Home Buying Journey Look Like in Walton County?

Most first-time buyers see the process in fragments. They hear “get pre-approved,” “tour homes,” and “show up at closing,” but they never get the full mission brief from curious stage to keys-in-hand.

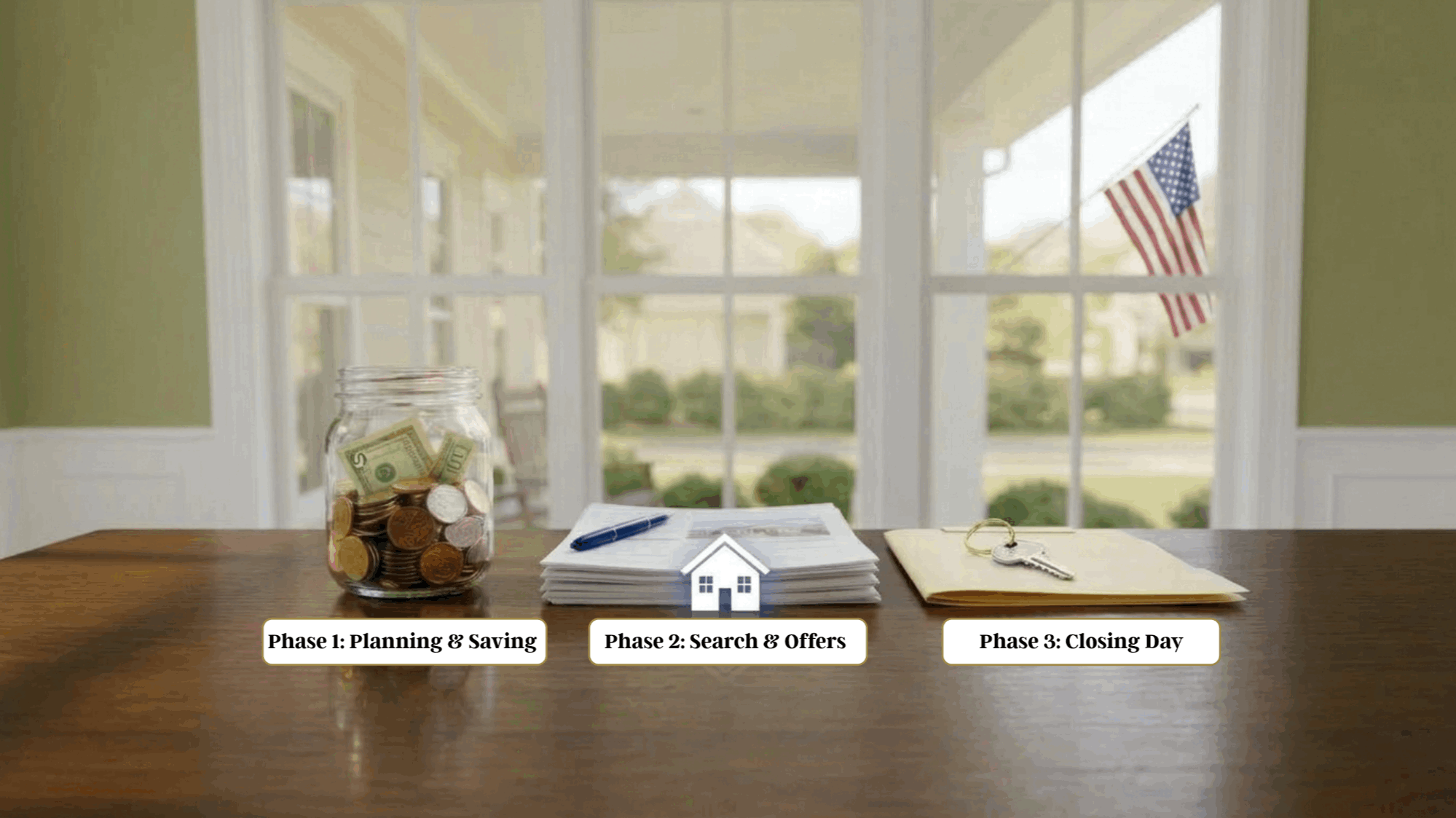

Simply put, the journey usually breaks into three big phases. Phase 1 is planning and money prep, which can take many buyers anywhere from about 1 to 6 months or longer depending on credit, savings, and how organized your documents are. Phase 2 is the home search and offer stage, which can often last 2 to 12 weeks but can move shorter or longer based on inventory, budget, and how selective you need to be. Phase 3 is the contract-to-closing stretch, which in many financed Georgia deals often runs about 30 to 45 days which can vary based on contract, lender, and several other factors.

That timeline is typical, not promised. Some buyers find a home fast and move cleanly through contract, while others need more time because of financing questions, inspection issues, or appraisal and title work.

If you’re asking, “How long does it take to buy a house in Walton County from first conversation to closing?” here’s the honest answer: in many cases, the biggest variable is not the closing table part. It’s how prepared you are before you start shopping.

A buyer who already knows the budget, has a real pre-approval, and has the right agent and lender bench can move much more calmly than a buyer who starts on Zillow and tries to build the plan backward. That is true in Walton or Barrow County, and really across Northeast Georgia.

If You’re Just Curious About Buying in Walton, What Should You Do First?

The first step is not touring houses. The first step is getting a money snapshot without judgment.

That means listing income, debts, monthly obligations, and current savings, then pulling your credit reports and checking for obvious errors. It also means thinking in terms of a comfortable monthly housing budget instead of the absolute maximum a lender might approve.

From there, a first-time buyer should do a rough rent-vs-own reality check. Not because owning is always better, but because ownership includes more than principal and interest; it also includes taxes, insurance, utilities, maintenance, and sometimes HOA dues.

A house fund matters early too. Even buyers using low-down-payment options often still need cash for inspections, earnest money, appraisal costs, and closing expenses, so starting that fund before shopping can take a lot of stress out of the process.

For many buyers, this curious stage can last 3 to 12 months. For others, a focused money and credit cleanup phase can take just a few weeks before they are ready to talk with lenders and move forward.

Walton County Reality Check: First-time buyers should watch local housing reports about typical price bands, days on market, and how competitive homes feel in the county. When we review MLS data together, we look at recent Walton and Barrow County examples so the conversation is based on current local snapshots, not old national headlines.

Any market snapshots or examples I share are based on MLS data at the time of writing and are for illustration only, not predictions or guarantees.

A good early education phase also includes learning the basic Georgia process, not just national advice. Georgia is an attorney-closing state, and that changes the closing experience in practical ways later.

It helps to understand the high‑level differences between common loan types so your conversations with a lender feel less intimidating; only the lender can walk you through which options fit your file. A first-time buyer does not need to become a mortgage expert, but understanding the basic difference between conventional, FHA, VA, and USDA can make lender conversations a lot less intimidating.

Some buyers explore state or local assistance programs—such as Georgia Dream or county‑level options—as examples, but availability and rules change. A participating lender and program administrator are the ones who can confirm current terms and whether you qualify.

Program availability, income limits, and benefit amounts can change without notice, and not all buyers qualify; only a participating lender and program administrator can confirm current details.

How Do You Choose the Right Lender and Get Truly Ready to Write Offers?

A strong first-time buyer usually talks with two or three lenders, not just the first person who answered the phone. That gives you a cleaner read on communication style, loan experience, timeline expectations, and whether that lender works with buyers in your price range and market.

The right lender bench for a first-time buyer in Walton County often includes someone who can explain options clearly, move quickly once you go under contract, and help you understand upfront costs before you fall in love with a house. The same logic applies in Barrow County, especially if your budget is tight and every dollar of cash to close matters.

Here’s the simple difference between prequalification and preapproval. Prequalification is usually a rough estimate based on self-reported information, while preapproval is a stronger lender review that typically includes documents, a credit pull, and a written letter showing a maximum loan amount and any conditions.

In 2026, serious home shopping usually starts with preapproval, not prequalification. Sellers and listing agents generally expect a true pre-approval letter before they take an offer seriously.

Only a lender can determine whether you qualify, what loan amount you may be approved for, and what actual rate, payment, and cost scenarios apply to your file. That line matters because real estate strategy and lending advice are not the same thing.

Questions you might ask every lender before you let them pull credit: ‘If there’s anything in my file that makes approval harder, what kinds of steps do buyers in my situation often take over time to get stronger?

A more thorough approval can also make your future offer more competitive and reduce surprises in underwriting. It does not guarantee a win, but it can make the process stronger and cleaner in many situations.

What Should a First-Time Buyer Expect from a Realtor in Walton County?

A good buyer’s agent should do more than unlock doors. A good buyer’s agent should help you understand the sequence, explain the contract deadlines, translate inspection findings into real decisions, and keep the process from turning into midnight panic-scrolling.

That starts with local experience. A first-time buyer should feel comfortable asking how often an agent works with first-time buyers, which parts of Walton County they know well, and how those areas differ in price, taxes, commute tradeoffs, and negotiation patterns.

Communication style matters just as much. You want to know how fast the agent typically responds, how showings are handled, what happens when a new listing pops up, and how updates are delivered once you are under contract.

A first‑time buyer should expect guidance that compares objective factors—price, taxes, commute, resale history, property condition, and contract terms—without steering based on protected characteristics.

This is where military-style clarity helps. My job is not to throw hype at a first-time buyer; my job is to help that buyer understand what to expect, what matters most, and where the actual risks live so the decision feels informed instead of rushed.

Helpful interview questions include:

☐ How will you explain each step from offer to closing?

☐ How do you help buyers compare neighborhoods in a fair-housing-safe way?

☐ How do you handle inspections and repair negotiations?

☐ How do you coordinate with lenders, inspectors, and closing attorneys when things get busy?

Once You Find “The One,” What Happens from Offer to Keys in Georgia?

Once you find the right house, the pace usually changes fast. The offer stage often moves in a matter of days, and then the contract becomes the timeline that drives everything else.

A Georgia offer usually includes the price, earnest money, financing type, closing date, due diligence period, contingencies, and any request for seller-paid closing costs. Contract date is effectively Day 0 for inspections, loan milestones, and the closing countdown.

Earnest money in Georgia is around 1 to 3 percent, in many cases, of the purchase price, although the exact amount is negotiable and contract-specific. In many cases it is held in escrow and credited back at closing if the deal closes according to the contract terms.

Due diligence is where a lot of first-time buyers either feel empowered or feel lost. In many Georgia deals, due diligence windows often land somewhere around 7 to 10 days, though some are shorter or longer depending on the property and market conditions.

That early window is when inspections should happen quickly. A general inspection usually comes first, and depending on the property, buyers may also add termite, septic, well, radon, roof, structural, or HVAC specialists.

Common inspection findings that deserve careful follow‑up with your inspector and, where appropriate, a contractor include: Active moisture issues, major roof age or failure signs, foundation movement clues, unsafe electrical concerns, HVAC systems near end of life, and septic or well problems on more rural properties deserve calm attention early, not wishful thinking late.

After inspections, a buyer may negotiate repairs, credits, or price adjustments within the contract timeline. In some situations, buyers and their advisors decide that a closing‑cost credit is cleaner than last‑minute repairs, because it lets the buyer choose contractors after closing.

While that is happening, the lender is moving the file through the full loan process. That usually includes updated documents, disclosures, appraisal ordering, and underwriting review.

Appraisals often come back within 1 to 3 weeks after order, and title work in Georgia is commonly handled by the closing attorney, who reviews ownership, liens, and document preparation. Many financed transactions reach clear to close in about 30 to 45 days if documents are provided quickly and no major issues surface.

Federal rules generally require the Closing Disclosure to be delivered at least 3 business days before consummation for most consumer mortgages. Then, usually within 24 to 48 hours before closing, the buyer does a final walk-through to confirm conditions and agreed work. Your lender and closing attorney are the authorities on how these federal timing rules apply to your specific loan.

Closing day in Georgia usually happens at the attorney’s office. Buyers sign the loan and title documents, funds are disbursed, and the deed is recorded, often the same day or next business day.

From “Just Curious” to the Closing Table, What Costs Should a First-Time Buyer Plan For?

Any numbers in this section are illustrations only, not quotes or guarantees. Only a licensed lender can provide actual rate, payment, and cost scenarios for your situation, and only your own professionals can tell you how those numbers apply to your contract and timeline.

The first cost bucket is early-stage prep. That can include optional credit monitoring, optional education or counseling, and in some cases a homebuyer education class if a lender or assistance program requires it.

The second bucket is cash due during contract. That often includes a general inspection, termite or pest inspection, any specialty inspections, and the appraisal fee if the lender collects it before closing.

In simple terms, buyers should expect many of those line items to be in the “few hundred dollars” range individually, with specialty inspections adding more as needed. Rural or more complex properties in parts of Walton or Barrow County can stack those costs faster than buyers expect.

Earnest money and, if used in the contract, a due diligence fee also belong in the cash-planning conversation. Earnest money is often around 1 to 3 percent in many Georgia transactions, and can vary by loan, price, and contract terms.

At the closing table, buyer closing costs in Georgia commonly land somewhere in the 2 to 5 percent range of the purchase price, and again, can vary by loan, price, and contract terms, separate from any down payment. Those costs often include lender fees, underwriting or origination charges, appraisal if not already paid, title work, attorney or settlement fees, recording fees, and prepaids like taxes and homeowners insurance.

Then there is the part many first-time buyers forget: the first year after closing. Even a move-in-ready home often needs some repairs, window coverings, tools, furniture, or basic maintenance spending once the seller is gone and real life kicks in.

A lot of planners suggest thinking about long-term maintenance in the range of roughly 1 to 3 percent of the home’s value per year, depending on age and condition. That is not a bill you pay on day one, but it is part of owning without getting blindsided later.

Cash to close is another phrase worth knowing. It generally means the total money needed at closing after credits, and it is different from down payment alone.

How Do You Avoid Rookie Mistakes That Cost First-Time Buyers Money and Sleep?

These are common patterns seen in many transactions; they are not personalized financial or legal advice. Your lender and attorney are the ones who can tell you how to handle your specific situation.

The first mistake is shopping at the lender max instead of your real-life comfort number. A lender may approve one ceiling, but your budget still has to cover groceries, utilities, maintenance, travel, childcare, giving, and whatever life throws at you.

The second mistake is treating prequalification like preapproval. In this market, that can lead buyers to chase houses they are not fully ready to buy or write offers that are weaker than they realize.

The third mistake is making big financial moves mid-loan. Many lenders caution that big financial changes during the process—new loans, job changes, large unexplained deposits—can cause avoidable issues, so buyers should check with their lender before making changes.

The fourth mistake is skipping the inspection in practice, even if you technically ordered one. A first-time buyer should attend the inspection, when possible, because that is where you learn how the house lives, not just what the PDF says.

The fifth mistake is missing contract deadlines. Inspection windows, financing deadlines, and appraisal-related decisions have real consequences, and missing them can cost leverage or, in some situations, put earnest money at risk.

The sixth mistake is assuming every issue has one clean solution. Low appraisals, title issues, repair requests, lender conditions, and seller negotiations can all be manageable, but they usually need a calm response and the right professionals involved early.

The seventh mistake is signing closing documents without reading the final numbers line by line with your closing attorney and lender. Buyers should compare the Closing Disclosure and settlement figures against earlier estimates and ask questions before closing day becomes a blur.

The specific rights and risks around earnest money, due diligence, financing, and appraisal depend on the exact contract language and Georgia law, so buyers should review these deadlines with their agent and closing attorney.

If you want the short version, here it is: get your money snapshot first, build the right lender bench, choose an agent who can explain the mission clearly, respect the contract timelines, and buy a home that fits your life instead of just your approval letter. That is how a first-time buyer in Walton County closes with eyes open instead of crossing fingers.

If you’re a first-time buyer in Walton County, Barrow County, or Oconee County and you want a step-by-step mission brief tailored to your timeline and comfort level, reach out to Fidelis Home Partners and I’ll walk it line by line from an educational and strategy standpoint so you can make decisions with your lender and attorney.

Nothing in this article creates an agency relationship or guarantees that any buyer or seller will achieve a particular result. Real estate markets, loan guidelines, timelines, and program rules can change without notice, so verify current market data, lending terms, and assistance details with your lender, closing attorney, tax professional, and other advisors before making decisions.

Recent Posts