Should I Sell My Home in Oconee County in 2026 or Wait? (A 3-Step Guide for Real Numbers, Not Headlines)

If you own a home in Oconee County and you’re deciding whether to sell in 2026 or wait, use a simple 3‑step filter: first your life timeline, then your equity and payment math, and finally your risk tolerance. In a slower, higher-priced Oconee market, you rarely get a perfect year—just a year that best lines up with your family and your finances.

You've probably seen the headlines. "Market cooling." "Rate lock keeps sellers stuck." "Crash incoming." Maybe you’ve even asked an AI whether you should sell now—but local decisions deserve local data and a real conversation. It's something trickier: a slower, more balanced environment where the right answer depends entirely on your life, your numbers, and your risk tolerance—not a national forecast designed for Phoenix or Tampa.

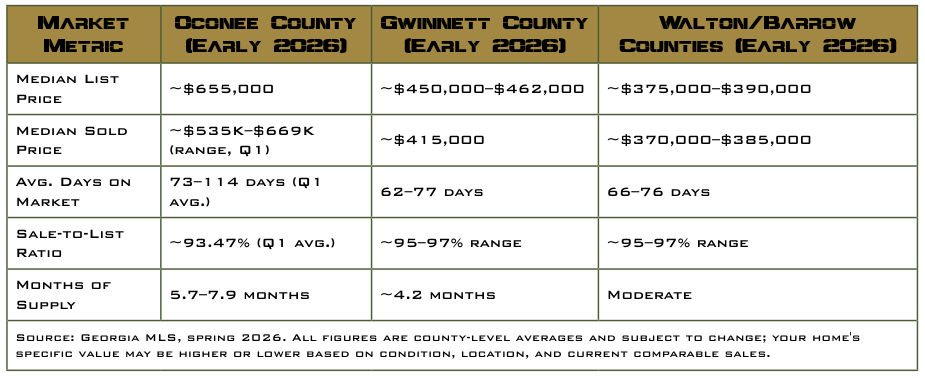

Here in Oconee, median list prices have held in the mid‑$600s—about $655,000 in March—while average days on market have stretched into the 70–110‑day range compared to much faster sales in 2024 (Georgia MLS, spring 2026). New listings are up more than 16% year-over-year, while closed sales are down. The question isn't whether to panic—it's whether your moment is now or later.

Everything here is for general education based on Georgia MLS and reputable public data as of spring 2026, and it is not legal, tax, or financial advice for your specific situation.

Step 1:

How Do Your Life Plans Shape Whether You Sell Your Oconee Home in 2026?

I’ve sat across the table from a lot of Oconee homeowners who think their decision is about the market when it’s really about what the next 12–24 months of life look like.

Major life changes—a job relocation, kids finishing at an Oconee school, a retirement window opening up, a caregiving situation shifting, a home that no longer fits—often dictate the real selling deadline more than any market forecast. A seller who knows they must move within 12–24 months has a completely different risk profile than someone who's flexible for years.

If you’ve spent months obsessively tracking rates and checking Zillow, that decision fatigue is a signal worth noticing. Selling a long-time Oconee family home takes emotional energy—decluttering, staging, showings, negotiations. If you’re emotionally ready, your next home is clear, and the numbers work, there’s real value in moving forward in a known 2026 environment instead of gambling on an unknown 2027.

Life Triggers Checklist

Run through these honestly. Multiple ‘yes’ answers tip toward a planned 2026 sale instead of waiting and hoping:

- Yes / No— Will your kids start or finish at an Oconee County school in the next 12–18 months, making a mid-year move awkward or costly?

- Yes / No— Is a PCS order, job change, or relocation likely within the next 1–2 years?

- Yes / No— Is your current home actively stressing your health, finances, or daily relationships—not just mildly inconvenient?

- Yes / No— Are you in a retirement window where rightsizing or relocating makes financial or lifestyle sense in the near term?

- Yes / No— Have you and your household clearly identified where you want to go next—and confirmed it's achievable at today's numbers?

- Yes / No— Is your current home a poor space fit—too much house, not enough house, or the wrong setup for where life is headed?

- Yes / No— Are you emotionally ready to go through the sale process this year, not just theoretically someday?

- Yes / No— Would staying in this home for another 2 years genuinely hurt your family's quality of life, not just delay a preference you’d like?

If you answered yes to four or more of these, life is already sending you signals. You don't need a perfect market to make a wise move.

These life-stage examples are for illustration only; before you make any move, we should look at your actual timing, goals, and numbers together, and you may also want to speak with your financial or tax professionals.

Step 2:

What Numbers Should You Run Before You Decide to Sell or Wait?

This is where many homeowners either get stuck in spreadsheet paralysis or skip the math and decide on gut alone—which rarely ends well. We’re going to use four simple questions and a clear‑eyed look at what Oconee’s 2026 market shows.

What Oconee's 2026 Market Really Feels Like

Based on Georgia MLS data through spring 2026, here's the honest picture:

Oconee is a higher‑end, slower‑moving market. List prices have held relatively firm, but buyers are negotiating harder—the sale‑to‑list ratio has dropped from 96.8% to 93.47%. On a $650,000 home, that’s roughly a $21,000 difference between list and sale, which is why pricing strategy matters.

Local numbers in this guide come from Georgia MLS and other reputable sources as of early 2026 and are always subject to change; your home's value and timing could be higher or lower based on its specific condition and location.

Three Numbers Every Oconee Seller Should Know Before Listing in 2026

-

- Your realistic net proceeds— Not your list price. Your likely sale price minus agent commission, closing costs, Georgia transfer tax, attorney fees, any concessions, and prep costs. This is the number that funds your next move.

- Your payment delta— Many Oconee owners have sub‑4% mortgages. Trading into a new mid‑6%‑range loan can change your payment significantly, so run that comparison before you decide.

- Your equity cushion— Owners who purchased in 2018–2019 may have seen 30–40%+ appreciation plus principal paydown, according to FHFA data. That equity can fund a move—or create tax questions worth reviewing with a CPA

The Four-Question Numbers Checklist

Before any serious listing conversation, work through these four questions:

- What is my likely sale price today? (Not what you want—what comparable homes are actually selling for in 2026 at the current list‑to‑sold ratio.)

- What would I net after all costs? (Commission, closing, attorney, prep, concessions, and carrying costs during 60–90+ days on market.)

- What does the next payment look like? (At current rate ranges and the price of your next home—run this as a hypothetical illustration with a lender, not a guess.)

- Are there any tax or capital-gains issues I should run by a CPA? (Federal exclusions exist for many primary-residence sellers—up to $250,000 for single filers and $500,000 for many married couples filing jointly, subject to IRS rules—but the details depend on your specific situation and how long you've owned.)

Illustrative example (hypothetical, not a quote or guarantee): Imagine an Oconee homeowner who bought in 2019 for $400,000 with a low‑rate mortgage. Today, comparable homes suggest a realistic sale near $600,000–$650,000. After roughly 8–10% in costs, they might net around $540,000–$585,000. Any numbers in this example are for illustration only and are not a quote or guarantee. Only a licensed lender can provide actual rate, payment, and cost scenarios for your situation.

If You Have a VA Loan on Your Oconee Home

This deserves its own attention. VA loans are often assumable by qualified buyers, meaning under certain conditions a buyer can take over your existing low-rate loan. In a market where new loans are in the mid‑6% range, a 2–4% assumable VA loan can be a powerful marketing tool that attracts more buyers and stronger terms.

But here’s the strategic layer most sellers miss: if a non‑veteran buyer assumes your VA loan without substituting their entitlement, some or all of yours may stay tied up, potentially limiting your next VA‑backed purchase. The decision isn’t just ‘can I use my loan as a selling tool?’—it’s ‘do I need my entitlement restored for my next move?

VA loan and entitlement rules are subject to VA guidelines and lender approval, and this section is not a substitute for advice from a VA-knowledgeable lender and your closing attorney. Always confirm how any assumption or sale would affect your eligibility and liability before you act.

Tax rules are complex and can change, and this is not tax advice; always confirm your potential capital-gains treatment and any other tax questions with a qualified CPA or tax advisor before deciding when to sell.

Step 3:

What Could Go Right—or Wrong—If You Sell Your Oconee Home Now vs. Waiting?

Step 3 is the honest risk conversation—not doom‑and‑gloom, not cheerleading, just a clear look at where each path can go sideways.

What the 2026 Market Risk Picture Actually Looks Like

If you sell in 2026 without a clear next-home plan, you could find yourself making a rushed purchase in a still-expensive rate environment—or paying Oconee-area rents (which are limited in supply and relatively expensive) while waiting for the right opportunity. Selling into a slower market is fine; selling without a clear next step is where problems start.

If you wait into 2027 or beyond, current forecasts point to modest statewide appreciation—low single digits annually—not a new wave of double-digit gains. For many Oconee sellers, waiting a year may add only a few percentage points to price—often offset by carrying costs, deferred maintenance, insurance, and property taxes. And if rates stay elevated or climb further, the buyer pool at Oconee's higher price points could shrink, extending days on market and increasing concession pressure.

If your home has aging systems—roof, HVAC, septic, well—that you've been managing around, waiting exposes you to a potential forced repair timeline before your next listing, effectively turning paper appreciation into a net wash.

No one can predict future home prices or mortgage rates with certainty; the scenarios in this guide are based on current forecasts and local patterns and should be treated as possibilities, not guarantees.

The Two-to-Three Scenario Paths

Here's how I'd frame the decision for most Oconee homeowners:

Scenario A — Sell with a plan in 2026:

If your life has a clear forcing function in the next 12–24 months (school transition, PCS, retirement, home no longer fits), AND your equity today is sufficient to fund the next step—this is likely your year. You’re selling into a known market, not gambling on an unknown 2027. Prepare thoroughly, price realistically, and count on 70–90+ days to contract. The number that matters is your net, not the list price.

Scenario B — Wait with clear eyes and a quarterly check-in:

If your life is genuinely stable, your payment is comfortable, and your home still mostly fits your needs—waiting is a rational choice. Waiting’ doesn’t mean ignoring the market. Set a quarterly review with your agent—current comps, days on market—and a trigger (equity level or life event) that moves you from ‘monitor’ to ‘list.’ Don’t wait passively; wait with intention.

Scenario C — Hold and rent (with realistic landlord math):

Some Oconee owners, especially those with low-rate loans and strong equity, are considering converting to a rental rather than selling. In a flat‑to‑modest appreciation environment, a well‑maintained Oconee home can make sense as a rental if the rent covers your total costs, you’re prepared for landlord responsibilities, and you’re comfortable tying up equity in one local asset.

Quick VA Questions to Ask Before You Sell Your Oconee Home

-

- Is my current VA loan more valuable as a tool for an assumable sale—or as a long-term rental asset?

- Do I need my full VA entitlement restored for my next purchase, or can I work with partial entitlement?

- If PCS or ETS orders are likely in the next 6–18 months, am I better off planning a deliberate 2026 sale than gambling on a rushed sale later under time pressure?

- Have I spoken with a VA-savvy lender about how any sale structure—assumption, conventional payoff, rental hold—affects my future VA eligibility and liability?

Here’s the veteran‑specific matrix most general real estate blogs never offer—because it takes real VA experience to know the right questions:

- PCS/ETS within 6–18 months + strong Oconee equity + school-zone location→ Lean toward a well-prepared 2026 sale. Selling under timeline pressure later costs more than accepting today's market with full preparation.

- Stable local employment + sub-4% VA loan + manageable payment + rental demand→ Consider holding as a rental, if you can be a real landlord and you've confirmed with a VA lender that holding doesn't compromise your next purchase strategy.

- Planning a VA purchase on your next home + currently holding a VA-backed Oconee home→ Talk to your lender first about how full versus partial entitlement affects your next purchase price ceiling before deciding whether to allow an assumption or structure a traditional sale.

VA loan and entitlement rules are subject to VA guidelines and lender approval, and this section is not a substitute for advice from a VA-knowledgeable lender and your closing attorney; always confirm how any assumption or sale would affect your eligibility and liability before you act.

Ready to Know Where You Stand?

The honest answer to ‘should I sell my Oconee County home in 2026 or wait?’ starts with your life, moves to your numbers, and ends with your risk tolerance. No headline or national forecast knows your Oconee equity, payment reality, or family calendar.

My role is to help you see your options clearly so you can decide if 2026 is the right move for your family and your equity.

If you want to start with a no‑pressure conversation, I can walk you through a personalized net sheet and equity review based on current Oconee comps—and if you’re a veteran, a straightforward VA strategy talk about what your entitlement picture looks like for the next move.

I'm a Marine Realtor helping veterans, homeowners, and first-time buyers build generational wealth through smart and simple home buying and selling strategies in Oconee, Walton, Barrow, and Gwinnett Counties, based in Watkinsville, GA.

If you want a personalized look at your options, I can walk you through local data and scenarios as your real estate advisor, but I will always encourage you to consult directly with your lender, CPA, and attorney before making final decisions.

Timothy Carithers | REALTOR® with Real Broker | ABR® | MRP | Master Certified VA Loan Specialist

4th-Generation Oconee County Native | Marine Veteran | Watkinsville, GA

📞 706.818.0813 | 🌐 Fidelishomepartners.com | ⭐ Google Business Profile

Nothing in this article creates an agency relationship or guarantees that any buyer or seller will achieve a particular result. Real estate markets change quickly, and all information here is subject to change without notice. Data points and examples are based on sources believed to be reliable as of spring 2026, including Georgia MLS and FHFA data, but you should verify current market statistics, loan guidelines, and program rules with your own professionals before making decisions.

Recent Posts