How Can Your VA Loan Offer Beat Cash and Conventional in Gwinnett County in 2026?

If you're a veteran buyer searching for a home in Gwinnett County right now, you've probably heard some version of this from a listing agent or seller: "We went with a stronger offer." And you're left wondering whether "stronger" means the other buyer's terms — or whether your VA loan just got quietly moved to the bottom of the pile.

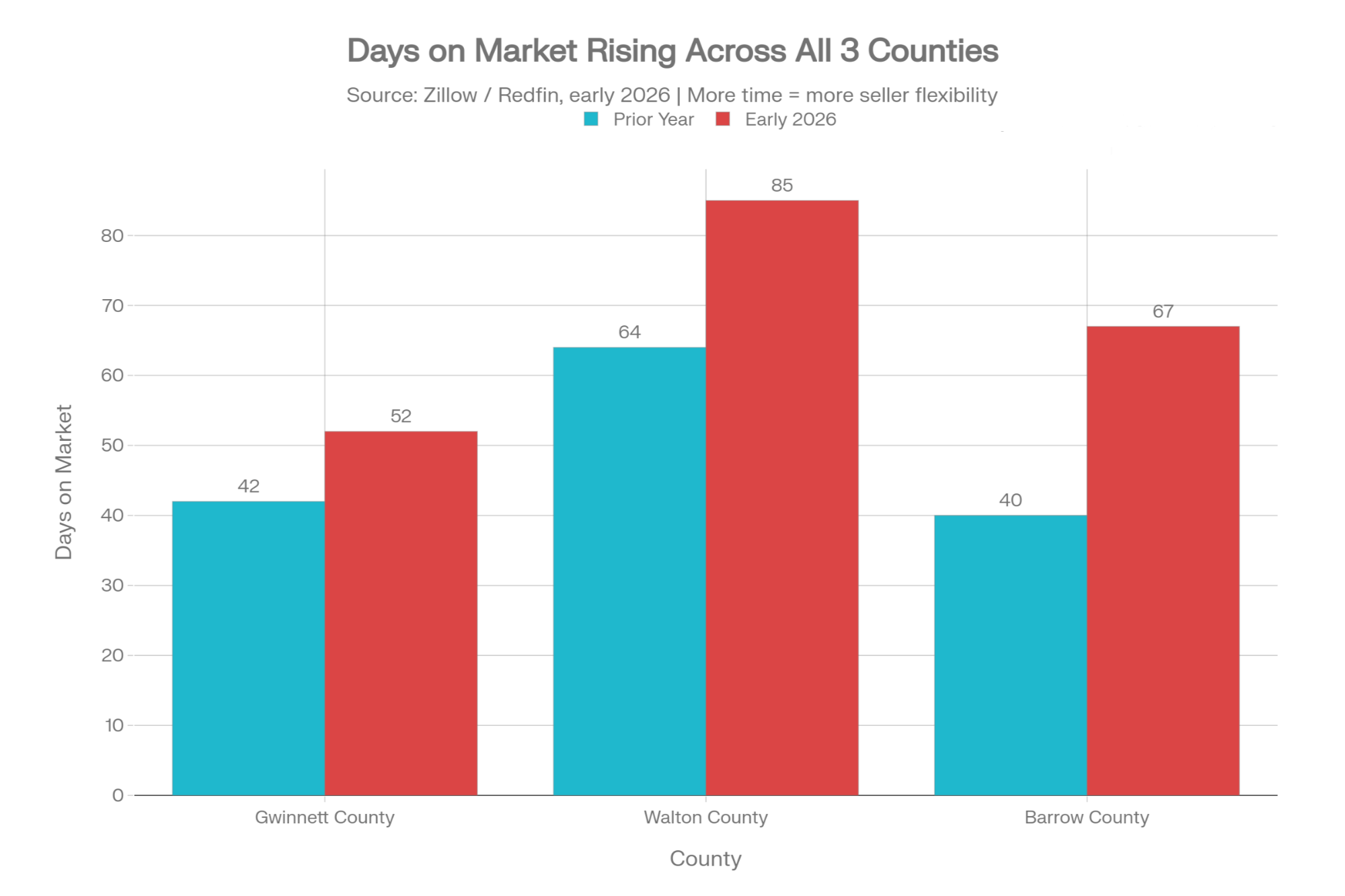

Here's the honest truth: Gwinnett's 2026 market is more balanced than it's been in years. Typical home values sit around $403,000–$419,000, homes are going pending in roughly 52 days — up about 25% from the prior year — and sellers aren't running twenty-offer bidding wars anymore. The playing field has shifted. But veterans are still losing deals in Gwinnett, Walton, and Barrow Counties — not because of their benefit, but because of old myths that refuse to die.

It should not feel like the benefit you earned in uniform is a disadvantage in Gwinnett. It isn't. You just need the right strategy and the right team behind you.

This article is for educational purposes only and is not legal, tax, or lending advice. Every buyer's situation is different. Always consult a VA-approved lender for rates, payments, and qualifications, and a real estate attorney or tax professional for questions about contracts, legal obligations, and taxes.

What's Really Going on in Gwinnett, Walton, and Barrow in 2026?

Gwinnett County is the main event here. Think about a veteran looking at a mid-$400s home in Lawrenceville that's been on the market six weeks — the seller is carrying that property and paying attention to every offer that comes in. A clean, certain contract from a fully prepared VA buyer is exactly what that seller needs right now.

Walton County, just west of Gwinnett, is what I'd call the calmer cousin. Average home values run around $378,000–$425,000, and days on market stretch from 50 to 85+ days in many areas — meaning more inventory and more room to negotiate. If you're a veteran eyeing a property in Loganville that's been sitting 60+ days, that seller has more motivation than their listing price suggests. A strong VA offer with the right structure can be very attractive here.

Barrow County is the stealth win. Typical home values around $347,000–$370,000, homes going pending in roughly 42–67 days, and months of supply that have climbed significantly — signaling more buyer leverage than this market has seen in years. Veterans willing to drive a few extra miles to Winder can often get more house, with more room to negotiate terms without sacrificing strength.

The short version: across all three counties, the real problem for veteran buyers isn't the market. It's the myths that follow the letters "VA" on an offer.

Why Do VA Buyers Still Lose to Cash and Conventional in 2026?

Four myths are doing most of the damage right now. Let's deal with them directly.

Myth 1: "VA loans take too long."

In many cases, when the file is well-prepared and the lender is experienced, VA loans can close in 30–45 days — often comparable to conventional. Delays typically come from incomplete documentation or property condition issues, not the VA program itself.

Myth 2: "VA appraisals always come in low and demand nitpicky repairs."

VA appraisals must confirm value and meet basic safety, soundness, and sanitation standards — exposed wiring, roof failure, structural hazards. They're not evaluating paint color or dated countertops. The biggest variable is the property, not the loan type. In many Gwinnett situations, a conventional appraisal on an overpriced home triggers the same kind of renegotiation.

Myth 3: "Zero down means no skin in the game."

Veterans still bring earnest money, pay for inspections, cover appraisals, and handle prepaids. The $0 down is a benefit — a strategic choice — not a sign of financial weakness. A veteran who keeps cash in reserves rather than tying it up in a down payment can often show more financial strength in an offer package than a conventional buyer who spent every dollar just getting to closing.

Myth 4: "Sellers always net less with VA."

Post-NAR settlement, commission structures apply regardless of loan type. VA loans don't automatically cost sellers more in 2026. This myth belongs in 2015, not today.

The villain here isn't your VA benefit — it's the misinformation surrounding it. And that's very fixable.

How Can a VA Buyer Look Just as Strong as Cash or Conventional in Gwinnett?

I'm a Marine Realtor helping veterans, homeowners, and first-time buyers build generational wealth through smart and simple home buying and selling strategies in Oconee, Walton, Barrow, and Gwinnett Counties, based in Watkinsville, GA.

Any examples in this article are illustrations, not offers to lend or guarantees that a particular strategy will be right for you. Only your lender can determine whether you qualify for a VA loan, what your rate and payment options look like, and how an appraisal-gap structure might work in your case.

Here's the 6-step tactical playbook I use with every VA buyer in these markets.

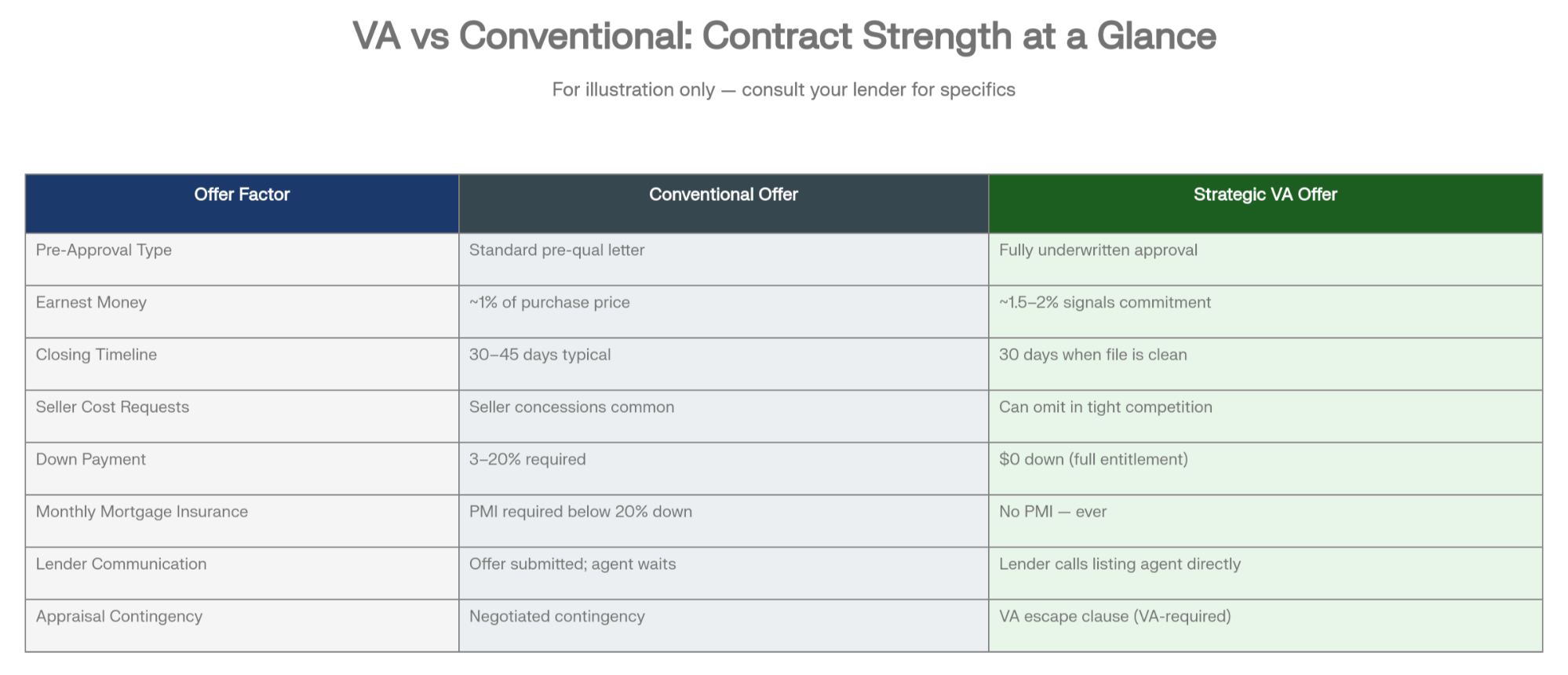

STEP 1: What Is a Fully Underwritten VA Approval, and Why Is It Your Golden Ticket?

There's a meaningful difference between a quick online pre-qualification and a fully underwritten VA pre-approval. With a fully underwritten approval, your income, assets, credit, and Certificate of Eligibility have already been through an underwriter — before you write a single offer. The file is mostly cleared.

To a Gwinnett listing agent, this changes the entire risk picture. Your offer doesn't say "maybe." It says this veteran is 90% of the way to the closing table before the ink dries. When most Gwinnett homes are going pending around 52 days, a VA buyer with a 30-day closing timeline doesn't look slow — it looks like exactly what the seller needs.

STEP 2: Why Does Your Lender's Name Matter as Much as Yours?

Here's a play I run on every offer submission: my lender partner doesn't just send over a pre-approval letter — they call the listing agent directly. They walk through the file strength, confirm the timeline, and address any appraisal expectations before the seller's agent even finishes reading the offer. That conversation has moved VA offers from the bottom of the pile to the top.

In Walton and Barrow Counties, listing agents may encounter fewer VA offers. When a local VA-first lender can point to a track record of 21–30 day closings on VA files in this specific market, that changes how the listing side reads your offer entirely. That's the name you want on your letter.

STEP 3: How Do You Structure a Financially Strong VA Contract Without Giving Up Your Protections?

Your VA benefit comes with real protections — the escape clause, zero PMI, occupancy requirements. What changes is how you signal financial strength through the contract structure itself. In many Gwinnett situations, here's what a stronger contract looks like:

- Earnest money around 1.5–2%instead of the bare minimum — VA loans don't require earnest money by rule, but serious earnest money tells the seller you have genuine skin in the game (any numbers here are illustrative — discuss with your lender what fits your situation)

- Tighter inspection windowswhen you've done homework on the property upfront, rather than using the inspection period as a back door

- Skip seller-paid closing costsin tight competitive situations when possible, or structure it so the seller doesn't feel like they're netting less

- Offer flexible possessionwhen the seller needs transition time — a 30-day post-closing occupancy arrangement can sometimes be worth more to a motivated seller than a higher offer price because it solves their real logistical problem (always work through your closing attorney on any occupancy terms)

"In a balanced Gwinnett market, sellers care more about

certainty than the letters 'VA' on the offer."

STEP 4: What's the Smart Way to Handle VA Appraisals and Potential Gaps?

Sellers and their agents often fear this: the VA appraisal comes in below contract price and the veteran walks. The VA Amendatory/Escape Clause protects veterans from being forced to buy a home above its appraised value — and that's a protection, not a problem.

For veterans who have reserves available, one strategic option is offering appraisal gap coverage up to a capped dollar amount. This tells the seller: if the appraisal comes in short, I'll cover up to $X of that gap out of pocket. It makes a VA offer look structurally more like a conventional offer in the seller's eyes, while still leaving room to walk if the gap becomes unreasonable. This approach needs to be worked through with both your lender and your closing attorney before it goes into a contract.

The VA Amendatory/Escape Clause and any appraisal-gap language in your contract involve legal rights and obligations. Always review these with your closing attorney so you understand how they apply to your specific purchase in Georgia.

STEP 5: How Do You Use Market Friction in Gwinnett, Walton, and Barrow to Your Advantage?

Not every situation calls for the same strategy, and knowing the submarket makes a real difference.

In Gwinnett, the higher-priced suburban areas — think Suwanee or the Peachtree Corners corridor, where mid-$500s to $700K+ move-up homes still see strong interest — appraisal gap language and tight contract terms matter most. Listing agents in those areas tend to understand VA; they just want certainty that a file will close.

In Walton, longer days-on-market (50–85+ days in many areas) mean a seller who's been carrying a listing for two months may value a committed VA buyer with a clean local lender over a conventional offer that's been shopped around.

In Barrow, rising supply and mid-$300s to $370,000 price points give VA buyers room to negotiate terms, sometimes even price — and still look like the strongest option in the building when earnest money and timeline are right.

"Your VA benefit is not the problem —

the myths about it are."

STEP 6: Why Does Communication Win Deals Before the Paperwork Gets There?

This is the part most VA buyers never hear about. When I submit an offer, I'm not just emailing a PDF and hoping it reads well. I'm running a briefing. My lender calls the listing side — before or immediately after submission — and walks through three things: file strength, expected timeline, and appraisal strategy. The listing agent understands what they're looking at, not as a sales pitch, but as a professional handoff of facts.

It's about the file being clean, the timeline being real, and the team knowing these specific markets. That changes how your offer lands.

"The right structure can make your VA offer look like 'cash with an appraisal' in the eyes of many Gwinnett sellers."

What Does Winning the Right Way Look Like for Veterans in Gwinnett?

Here's what this looks like in practice. A veteran buyer comes to me eyeing a mid-$400s home in a Gwinnett neighborhood that's been on the market about 50 days. We get a fully underwritten VA approval in hand, structure an offer with around 1.5–2% earnest money, a clean inspection timeline, and no seller-paid closing cost request. My lender calls the listing agent the morning the offer lands. The seller — weighing a conventional offer at a slightly higher price — chooses the VA buyer. Because certainty and clean terms matter more than the extra few thousand dollars when you've been carrying a listing for seven weeks. (This is a composite illustration; individual results will vary.)

That's not a miracle. It's a repeatable process built on preparation and the right team.

If you're an agent outside Gwinnett with a veteran buyer heading this way, let's connect. I'm MRP and ABR designated, Master Certified in VA loans, and I work these three counties regularly — I know how listing agents here think about VA offers.

Frequently Asked Questions About VA Offers in Gwinnett County

Can VA buyers still lose to cash offers in Gwinnett County in 2026?

Yes — but in most cases, it's not the loan type. It's the structure. A fully underwritten approval, strong earnest money, tight terms, and a lender who picks up the phone can make a VA offer more competitive with cash in Gwinnett's 2026 market.

How fast can a VA loan close in Gwinnett today?

When the file is prepared and the lender knows VA, closings in 30–45 days are common — sometimes faster. The key variables are documentation and property condition, not the loan type. A local VA-first lender with a Gwinnett track record can give you a realistic timeline for your situation.

Do sellers in Walton or Barrow County prefer cash over VA?

Some do — still running on outdated assumptions. But with days on market rising and inventory climbing in both counties, a committed VA buyer with clean terms and a local lender often beats a cash investor who's going to renegotiate after inspection. That narrative changes with education and a direct conversation.

Nothing in this article creates an agency relationship or guarantees that any buyer or seller will achieve a particular result. Real estate markets change quickly, and all information here is subject to change without notice. Data points and examples are based on sources believed to be reliable as of early 2026, but you should verify current market statistics, loan guidelines, and program rules with your own professionals before making decisions.

Recent Posts