Is Barrow County Still Affordable for First-Time Homebuyers in 2026? A Reality Check on Prices, Payments, and Options

Headlines scream more inventory and softening prices across East Metro Atlanta, but first-time buyers still feel the pinch from high monthly payments. You're not imagining it—rates remain elevated, and even flat prices mean today's math doesn't match 2021 dreams. Barrow County often stands out as one of the more accessible entry points on this side of town, but only if you have clear numbers, a simple plan, and someone willing to walk you through both with no pressure.

I’m a Marine Realtor based in Watkinsville, helping veterans, homeowners, and first-time buyers in Barrow, Walton, Oconee, and Gwinnett Counties build generational wealth through smart and simple home buying and selling strategies.

A simple way to think about it is to start with your monthly comfort band, then reverse‑engineer the price range instead of chasing a number you saw online. Many first-time buyers I meet in Barrow feel best when their total housing cost fits alongside real life—emergencies, kids’ activities, and other bills. I encourage buyers to work with a local lender to define a comfortable and a stretch payment, then I match that pre‑approved budget to what’s actually available in Barrow at those price bands.

What Does “Affordable” Mean for First-Time Buyers?

Affordable means a comfortable monthly payment relative to your income, not just the sticker price on a house. In Barrow County as of early 2026, this focuses on total housing costs fitting your budget without constant stress.

Nationally, payments have risen sharply since the low-rate years, even in places where prices are flat. The key insight: affordability sits on a spectrum tuned by three dials—price, rates, and structure (loan types, buydowns, and concessions). First-timers often fixate on price alone and miss how tweaking the other two can sometimes shift “no way” to “maybe.”

"Quick Visual: The Three Affordability Dials

- Price: What you agree to pay for the home.

- Rate: The cost of borrowing that money.

- Structure: How the loan, buydowns, and seller concessions are put together.

Most first-time buyers only watch price. In 2026, structure is often where the real leverage lives."

Barrow County Prices in 2026

Based on Georgia MLS as of March 2026, Barrow’s median sold price was approximately $375,000. Year‑over‑year changes in January 2026 were up about 4.1%, and in February 2026 were down about 14.1%.

Recent MLS data shows days on market stretching to roughly 50–75 days, with more inventory and price reductions—nearly 40% of listings have seen price cuts and many sale‑to‑list ratios are under 100% as of early 2026, all subject to change.

More Affordable Than Neighbors?

Market figures are approximate based on Georgia MLS as of March 2026 and are subject to change.

Always confirm current data with your agent and lender.

Barrow typically lands one affordability step below Walton and Gwinnett, well under Oconee, especially factoring taxes and insurance qualitatively. For buyers trading commute for lower payments, Barrow sometimes turns "no way" into "maybe" or possibly a "yes."

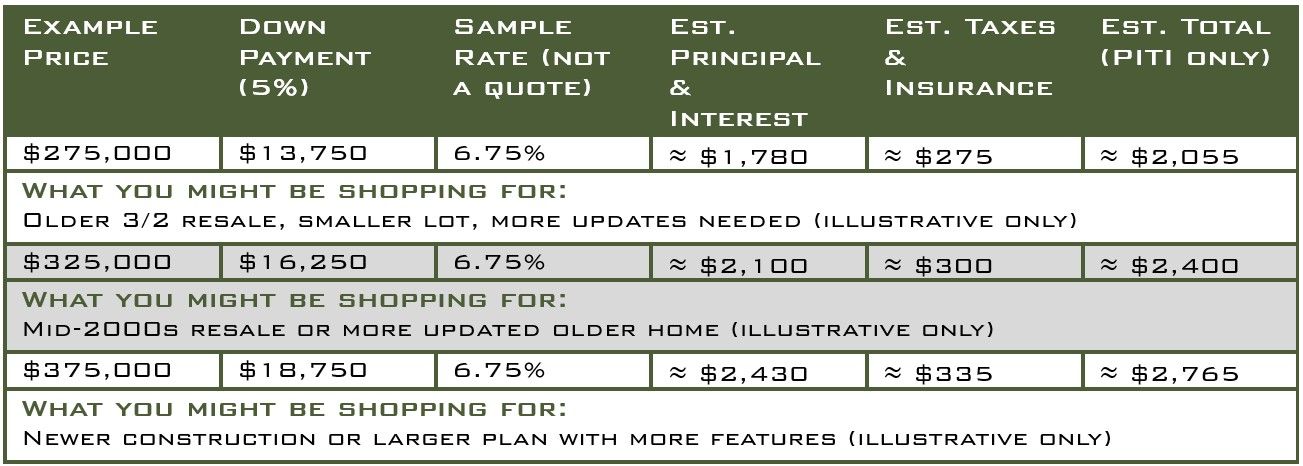

Here’s a rough illustration of three different sample price points in Barrow using a single sample interest rate and rounded estimates for taxes and insurance. This is not a quote—your lender will calculate your actual numbers.

Sample scenario: 5% down, 30‑year fixed, 6.75% sample interest rate (not an offer to lend), owner‑occupied single‑family home.

These examples are meant to give you a feel for how price bands can line up with monthly payments in Barrow,

not to predict what you personally will qualify for.

Actual options will depend on property type, condition, and what’s on the market when you buy.

Mortgage Illustration Disclaimer: These calculations are simplified examples only and do not reflect actual loan offers. For accurate payment calculations and pre‑qualification, contact a licensed mortgage lender.

What Can Buyers Actually Get?

Practical on-ramps include older 3/2 resales in mid-$200s to low-$300s based on condition and spot, as of early 2026. Newer/smaller construction hits higher $300s to low $400s, often with builder incentives. Non-traditional options like manufactured or rural properties dip below median where financing fits.

Realtor tip:

Consider targeting stale listings, price‑reduced homes, or fall‑throughs as places where sellers may be more flexible on price or concessions; this is an illustrative example only, not a guarantee.

In many cases in Barrow, I see value in the ‘ugly but solid’ homes that need cosmetic updates more than major repairs. A late‑1990s or early‑2000s 3‑bedroom resale a few miles from the newest subdivision may price under a shiny new build but live almost the same once you’ve painted, swapped flooring, and updated a few fixtures. For a first-time buyer who’s handy or willing to tackle projects over time, that trade-off can mean a lower purchase price today and more room in the budget for improvements later, instead of paying a premium for someone else’s choices.

I also see buyers win in Barrow by being flexible on square footage and lot size. Some builders still offer smaller floor plans or more basic finish packages that keep pricing closer to the low‑$300s to mid‑$300s when incentives are factored in, even as larger plans push higher. If your priority is getting into a solid starter home and starting to build equity, being open to a slightly smaller house or simpler finishes can open doors that look closed at the median price point.

Payments, Concessions, Programs in 2026

Many Barrow deals on longer-sitting homes include seller help like closing costs, repairs, or buydowns; a temporary or permanent buydown can ease payments from “no” to “stretch”—structure often matters more than the headline rate.

High-level aids: programs such as Georgia Dream or USDA may be available depending on income, location, and lender guidelines. A local lender can confirm whether you qualify. Buyers over-focus down payments, underuse concessions/programs shifting cash and costs.

Mortgage Payment Disclaimer: The payment calculations shown are illustrative examples using standard amortization formulas and do not reflect actual loan quotes. Your actual monthly payment will vary based on your credit score, down payment amount, loan type, lender fees, property taxes, homeowners’ insurance, HOA dues, PMI if applicable, and current market rates at time of loan lock. These examples do not include closing costs, prepaid expenses, or escrow requirements. For accurate payment calculations and pre-qualification, contact a licensed mortgage lender.

Buyer Questions in 2026

Is Barrow still cheaper than Gwinnett? Typically yes on price, with less competition for many entry-level homes. Can you still find something under the low $300s? Sometimes, with older resales or more non‑traditional options, but expect trade‑offs and talk with your lender about financing requirements.

5-Step Marine Plan for Barrow First-Time Buyers

This is the same simple, disciplined process I walk my own first-time buyers through in Barrow, Walton, Oconee, and Gwinnett.

Next Steps for Barrow Buyers

Here's a 5-step, Marine-precision plan:

1. With your lender, define a comfortable and a stretch payment, then back into a realistic price band from that budget.

2. Pre-approve with a local lender versed in VA, USDA, and Georgia Dream.

3. I pull Barrow targets under your pre‑approved price band—often below the current median, 30+ days on market, or recently reduced.

4. Compare Barrow vs. Walton/Gwinnett side-by-side for payment trade-offs.

5. Write a strong, data‑driven first offer that still leaves room for negotiation on concessions, timing, and buydowns.

When we walk through this together, we’re not just checking boxes—we’re building a decision you can explain to yourself six months later and still feel good about, because you understand the numbers and the trade-offs up front. I’ll show you how Barrow, Walton, and Gwinnett stack up for your specific budget, commute range, and timeline so you can see, in black and white, where the trade‑offs actually are instead of relying on headlines or hearsay.

Request your free "Barrow First-Time Buyer Reality Check"—I'll run your numbers, price band, and 3 affordability boosts (concessions, programs, choices). No pressure, data-driven only. This review is informational only and does not create a client relationship until we both sign a written agreement, as required under current real estate rules.

As a Marine Realtor based in Watkinsville, serving Barrow, Walton, Oconee, and Gwinnett, my job is to give you clear, data-driven options so you can make a confident first-time buying decision that fits your life and your long-term goals.

Legal/Financial Disclaimer: This blog is for educational purposes only and reflects my experience as a licensed Georgia real estate agent; it is not legal, tax, or financial advice, and it is not a commitment to lend.

Recent Posts